Over six months have gone by since I last negotiated our internet rates with Comcast (see here). Our 25 Mbps (mega bit per second) connection went from the promo price of $35/month to $67. I tried calling in late December to get rolled over to a new promotion. Like always, I call in and navigate the voice menu to canceling all services. That lands you into their customer retention department and the best possible deals.

The rep offered $50/mo for internet and phone service. I really didn’t want to add a service that we are not going to use and the price is still about $10 more than what I want to pay so I declined.

Comcast runs new promos every 30 or so days, so I gave them a call back at the start of January to see if they had anything new. This rep offered $55 for internet and basic cable. An even worse deal in my opinion. She also offered a $40/mo for internet only, but it was a meager 6mbps. The only competitor in town has that same level of service for $30.

Again I declined, and figured I would call back in a day or two (the second rep was not very friendly).

This afternoon, I called for a third time, persistence is key! I got the first offer again, phone + internet for $50. I agreed, and have set a reminder on my calendar to try again in February.

The new deal is good for 12 months and will save us $204 over what we have now for the same level of service. It is not a particularly great deal, but it beats the standard rate and matches the competitors price without the hassle of moving accounts. Sometimes we just have to take the small wins. :-\

This morning while Frugal Boy was napping, we broke out our pasta roller and ravioli maker gadgets to try our hand at making homemade ravioli. Both were recent gifts and since we love pasta, especially ravioli, we determined that it was time to put them to use.

Technically, we had already made an attempt on Thursday, one that ended in complete failure. There are a lot of different recipes for a basic egg pasta and the first one that we followed had to be salvaged into wide lasagna noodles. After a couple of days and some advice from Peter Pasta’s youtube videos, we tried a different, simpler recipe.

Voila, super easy and beautiful looking ravioli!

The little squares are text book perfect. 😀

We used a basic ricotta, mozzarella, and Italian seasoning filling. The booklet that came with the attachments had some delicious sounding recipes that we will have to try out in the future.

You can either cook, refrigerate, or freeze your finished ravioli after making them. Ours are sitting in the refrigerator and we’ll boil them up for dinner tonight.

Our dough recipe was extremely simple.

2 cups flour

2 eggs

water

Dump the flour and eggs into a mixer. Use the flat beater to mix the ingredients together. One of our mistakes the first time was we tried to use the dough hook. Finally, add in water as needed to get to the right consistency. There should be small clumps/flakes and if you squeeze it in your hand, it should not fall apart.

Peter Pasta’s spaghetti video shows how to make the perfect egg pasta dough in preparation for ravioli.

He skips the dough preparation in his ravioli video (marketing his brand of pre-prepared dough mix).

I did some back of the envelope calculations and our homemade ravioli is about 1/2 to 3/5 the price of store bought. The filling is easily the most expensive part. If you make and eat a LOT of ravioli, these attachments might be frugal. One thing is for sure, they are super fun! We’re already thinking of all the different types of fillings and doughs that we can make.

Pumpkin-Sage Ravioli with Browned Butter and Pecans

Salmon Cream Cheese Ravioli with Roasted Garlic Cream Sauce

Chicken, Pine Nut, and Goat Cheese Ravioli with Traditional Red Sauce

Spinach and Mushroom Ravioli with Roasted Red Pepper Cream Sauce

Happy New Years! Here is a recap of our 2014 in numbers

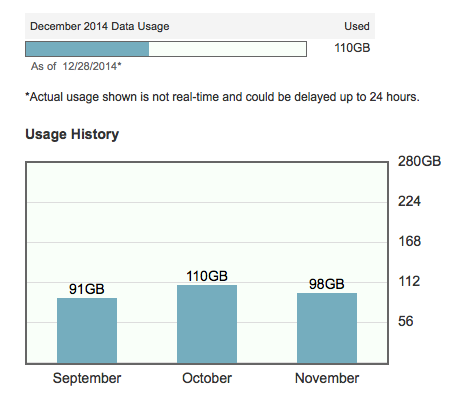

1,224 GB Data Used

While I don’t have full usage history for our internet connection, I do have the past four months. If I extrapolate that data then I can summarize that we have used on average about 102 GB of bandwidth each month in 2014. Most of that is probably Netflix related. In total we spent $399.78 for internet in 2014, or 32¢/GB. You can read more about trimming your bill here and here.

1,140 CCFs (852,000 gallons) of Natural Gas

Our furnace, water heater, and oven all use natural gas. Heating continues to be the number one demand for gas in our household. 1 CCF is 100 cubic feet or the equivalent of 748 US gallons. An olympic swimming pool holds 660,000 gallons. We couldn’t quite trap all of the natural gas we used this year in an olympic sized swimming pool.

Insulating (part 1 and part 2) our house will hopefully conserve more resources in the future. Our main enemy are our leaky windows (temporary fix).

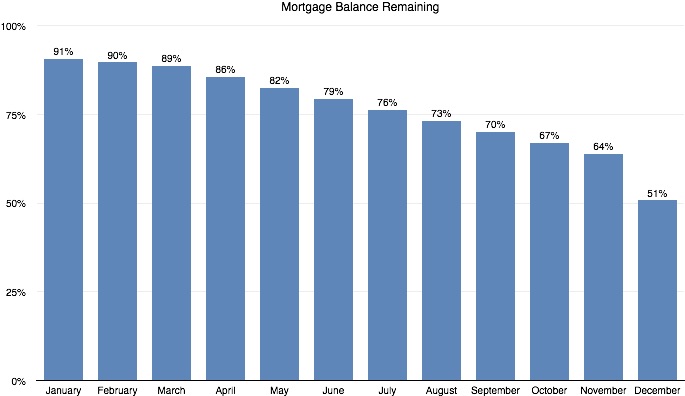

40%

Is the amount that we have trimmed off our mortgage principal. We started making quadruple payments in April and are motivated to be mortgage free by the end of next year. Living frugally and skimping on gifts to ourselves has helped (see frugal gift ideas here). Debt is an emergency!

18,700 Gallons of Water (2,500 cf)

That is about three milk tankers.

According to the EPA, the average American uses between 80-100 gallons of water a day. Thanks to the installation of low flow faucet aerators (here) and low flow toilets (here and here), we averaged about 25 gallons per person (with Frugal Boy included it would be about 17 gallons).

5,514 kWh of Electricity

According to the US Energy Information Administration, the average household uses 10,837 kWh a year. We came in about half of that thanks to using CFL and LED lightbulbs instead of incandescent. We also use the low heat setting for our dishwasher and try to turn off lights and other energy suckers when they are not in use. Our total electric bill for the year came out to be $652.92. $49 of that was just to have service provided.

$36,757.30 in Medical Bills

Having a baby is expensive, especially when things don’t go according to plan. Having good insurance and understanding what it covers means that we only paid $387.98 out of pocket. That was even with the highest deductible plan. Health Savings Accounts, HSAs, are awesome (especially when it is employer money)!

7

The number of states we visited this year. Read more about it here, here, and here.

I was too lazy to make a new map showing Wisconsin as visited, just take my word for it

8

The number of teeth that Frugal Boy has. Aye aye aye!!!

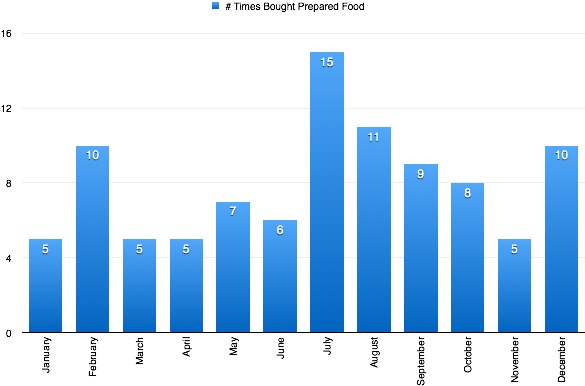

96

The number of times we bought prepared food (restaurants, take out, forgot to pack a lunch, anything except the grocery store). February we had a baby and grabbed more than one lunch/dinner from the sandwich shop. July and September we went on semi long road trips. Maybe a good challenge for 2015 would be to go a month without going out.

1,320 Minutes Talking on the Phone (Andrew)

According to the little statistics screen on my phone, I blabbed for about 22 hours in 2014.

1,083 Blog Visits

Google Analytics tells me that is how many sessions (not to be confused with page views) that this blog has had in 2014. 90% of those visitors are from the good ole United State of America. 7.5% are from Russia (hey leave a message, assuming you aren’t a bot), and the rest are scattered about.

2,157 Spam Comments Blocked

You may have noticed that you can no longer comment on older articles. That is my attempt to cut down on spam. Thankfully I have to do virtually no work to manually eliminate the junk because of the wonderful Akismet wordpress plugin.

2015

The number of roads a man must walk down or maybe just another good year. Enjoy and live frugally!

You probably know who Warren Buffet is, but do you know about John Bogle? If you invest through Vanguard then you should, because John Bogle was the pioneer of low cost index funds. In his book, John Bogle on Investing: The First 50 Years, he presents a collection of essays and speeches that discuss the founding principles of Vanguard and why those principles are just as important today as they were 50 years ago.

Simplicity

Bogle argues again and again that simplicity is favorable over complex investing strategies time and time again. The more complicated you make investing, the harder it is to understand and the easier it is to get caught up and make a mistake. Why go to the trouble of sorting through a haystack to find a needle when you can just buy the entire haystack. In his opinion, instead of trying to pick winners (needles) out of the stock market, just buy the entire stock market (the haystack). The simple goal of enjoying the entire market return in aggregate will statistically beat the complicated goal of trying to outperform the market by identifying the best stocks.

Long Term Investing

The longer the time horizon is for the investment, the better it will do. While stocks are more volatile than bonds, over a 25 year horizon that increased volatility drops to a standard deviation of just 2% of a 6.7% median return (meaning that you could expect returns between 4.7% and 8.7% with a degree of confidence). Compare that to the one year deviation of 18.1% on 7% median return (-11.1% to 25.1%) and you can see how the longer you hold an equity the more the peaks and valleys are smoothed out. Just like Buffet, Bogle takes a buy and hold mentality.

Costs Matter

Vanguard is unique among brokerages because it is a mutual company. When you buy a Vanguard fund, you become a part owner of the company. The advantage of this over a private company, is that Vanguard wants to better serve its masters, and those masters are fund holders. What do fund holders want, lower costs!

Consider the two scenarios below. One portfolio has a 1.2% expense ratio, the second has a 0.2% expense ratio.

Now which expense ratio would you rather have? Cost is one parameter that investors can control!

Index vs Actively Managed Funds

An actively managed fund has a human being or a whole team of humans that are trying to pick winners for a fund. They eat, sleep, and breath financial markets. Why try and choose winners yourself when you can let a team of experts do it for you? The answer is that you shouldn’t let the ‘experts’ do it for you because historically they have been outperformed time and time again by index funds. Index funds are passively organized to track a benchmark. A common example would be an index fund that recreates the S&P 500. Index funds can pass cost savings, by not having to pay a salary to an expert, to you, the person who is risking their hard earned money.

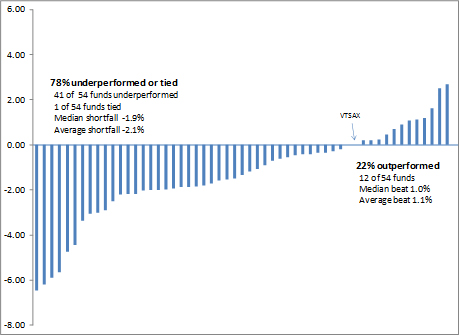

Bogle loves to tear apart actively managed funds in his book by showing cold hard numbers again and again. The numbers don’t lie, actively managed funds underperform. Just take a look at this analysis done by Forbes.

Using VTSAX, Vanguard Total Stock Market Index Fund, as the baseline, they compared 54 actively managed funds that had the same investment objective. 78% of those actively managed funds posted returns less than the passive index fund. Only 22% outperformed VTSAX. If I approached you and said you had a one in five chance of beating the market, would you bet the farm on it? If so, please don’t go to Vegas, they’d love you.

Conclusion

The book is quite long and not for the new investor. If you are interested in getting started in investing (you should be!) then I would recommend that you check out Vanguard’s 4 Principles for Investing Success on their website. Then use Vanguard’s Portfolio builder to get a recommendation that is personalized to your situation.

We will be reorganizing our taxable investment account in January to better align with Bogle’s and by extension Vanguard’s philosophies. For starters, we will be simplifying our positions from:

VCR – Vanguard Consumer Discretionary ETF (expense ratio 0.14%)

VDC – Vanguard Consumer Staples ETF (expense ratio 0.14%)

VWO – Vanguard FTSE Emerging Markets ETF (expense ratio 0.15%)

VYM – Vanguard High Dividend Yield ETF (expense ratio 0.10%)

VCSH – Vanguard Short Term Corp Bond ETF (expense ratio 0.12%)

VBK – Vanguard Small Cap Growth ETF (expense ratio 0.09%)

AAPL

To:

VTSAX – Vanguard Total Stock Market Index Fund Admiral Shares (expense ratio 0.05%)

By switching from ETFs to a mutual fund, we are simplifying our contributions. In the future we will be able to setup a monthly direct deposit directly into VTSAX instead of transferring money into our account and manually placing buy orders for each ETF.

We will also be reducing our cost. 0.05% expense ratio is an incredible value!

You may be wondering about diversification. Well, VTSAX, with 3804 holdings, gives us ownership in virtually every publicly traded company in America. We’re buying the haystack. Our prepayments on our mortgage serve as our ‘bond’ replacement, and I am not convinced that in our investment horizon (20+ years), foreign equity or bonds are needed at this time.

So there you have it. Our low cost, indexed, long term, and easy to understand investment portfolio. It consists of buying and holding a single mutual fund. What could be easier than that?

If you are just getting started VTSMX is the same thing as VTSAX except it has a lower initial investment requirement and a slightly higher expense ratio. VTI is the etf version.

This is the last weekend before Christmas and because it was a bit chilly to walk outside with Frugal Boy I braved the mall. No, I’m not a masochist, I just know that Frugal Boy loves people watching and what better place is there to people watch than the mall before Christmas.

As I was unloading the stroller back at home, one of our neighbors came by and asked if I had finished my Christmas shopping. I told him no, I had never even started. He offered me luck on a seemingly impossible task, to save Christmas in less than a week. What I didn’t tell him, was that while I hadn’t done any traditional shopping, I was in fact done with gift giving.

The Frugal Gift For Your Spouse

Shae and I have always had an aversion to trying to find the ‘perfect’ gift for one another. The hassle of it all, shopping, buying, wrapping, keeping the secret, and hoping for a genuine positive reaction during the unveiling is all a bit more work than either of us would like to do. In something of a growing tradition, the goto token gift has become new pairs of socks, simple, practical, and fairly cheap.

Our unconventional gifts to one another are both easy to give and a joy to receive. This year we both paid off a chunk of our mortgage for a combined extra prepayment of 10%. All told, in 2014 by living frugally, we have been able to shave off 40% of our mortgage this year alone.

10% Christmas Gift to Ourselves

The quadruple mortgage payments that we started making in April have set us on track to be mortgage free in about 12 months (assuming we give ourselves the same present next year)! Yippee!

The Frugal Gift For Your Child(ren)

Frugal Boy isn’t old enough to really appreciate presents, so this year we just made a contribution to his 529, college savings, plan.

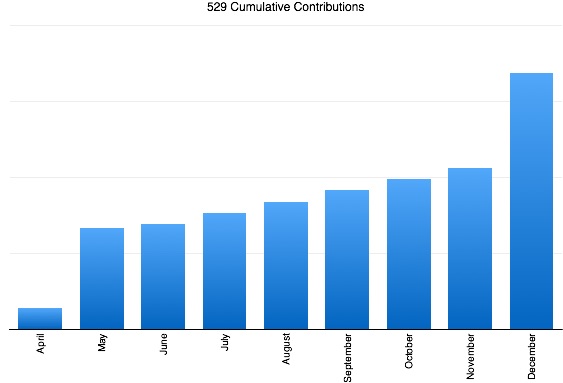

Merry Christmas Son

You can see two jumps in the chart. The first in May when we put inheritance money towards future education and another in December when we gave him his present early.

While a 100% monetary gift works well for babies, because they don’t understand the concept of a gift, it probably won’t be a smash hit with older children. In the future we will continue to spend a substantial amount of Frugal Boy’s gift budget on 529/savings contributions while spending a bit of money on a token toy. After all, as parents, it is our job to take care of the needs and necessities first. We can let his relatives spoil him with the ‘fun’ stuff. If our Christmas tree is any indication, that is exactly what is happening (100% of the presents are to Frugal Boy).

The Frugal Gift For Your Nieces and Nephews

We basically followed our standard method of operation for our own children. Babies received all cash gifts and should their parents choose to invest that money in an account that compounds that niece or nephew will receive the advantage of time. Older nieces and nephews received trinkets and a supplement of cash to round out their presents. As an uncle and an aunt, we tend to be more prone to spoiling than with our own child. Plus, what kid doesn’t want 1,000 stickers for Christmas? 😀

Wrapping Up

While we haven’t done the traditional gift giving this year, we have done a frugal edition of it. A grand total of zero items were purchased at the mall, and most gifts came from our checkbook. Sure it isn’t the picturesque Christmas that you see in the films, but then again is that even the meaning of Christmas in the first place? With that said, are you done with your Christmas shopping?