My photo library has a bunch of pictures that don’t warrant individual posts, so today is a potpourri day.

The weather here has finally gotten above freezing. Frugal Boy only had a brief encounter with snow this winter (fingers crossed we don’t get slugged with a giant blizzard in the last 1.5 months of winter).

Shae tried her hand at making and freezing breakfast sandwiches. It is nice to have a quick hot breakfast on cold mornings. Aldi is the cheapest grocer that we have found for pre-made sandwiches, 75¢/sandwich. Ours are about equal in price.

Shae also managed to sell Frugal Boy’s Bumbo chair for $14. We paid $5 for it at a garage sale.

The grandparents visited for a few days. It is always nice to have extra hands and eyes to corral youngins.

Yesterday we did some Spring cleaning. If I call it that, will it make it Spring? Living with 24 pounds of curiosity is a great motivator to declutter and clean.

Quick, hop in this time machine and I will take you back to the day that Shae and I got married.

BEE BOO BOP! Ding!!

We’re there. Take a look at that young couple enjoying the summer sun.

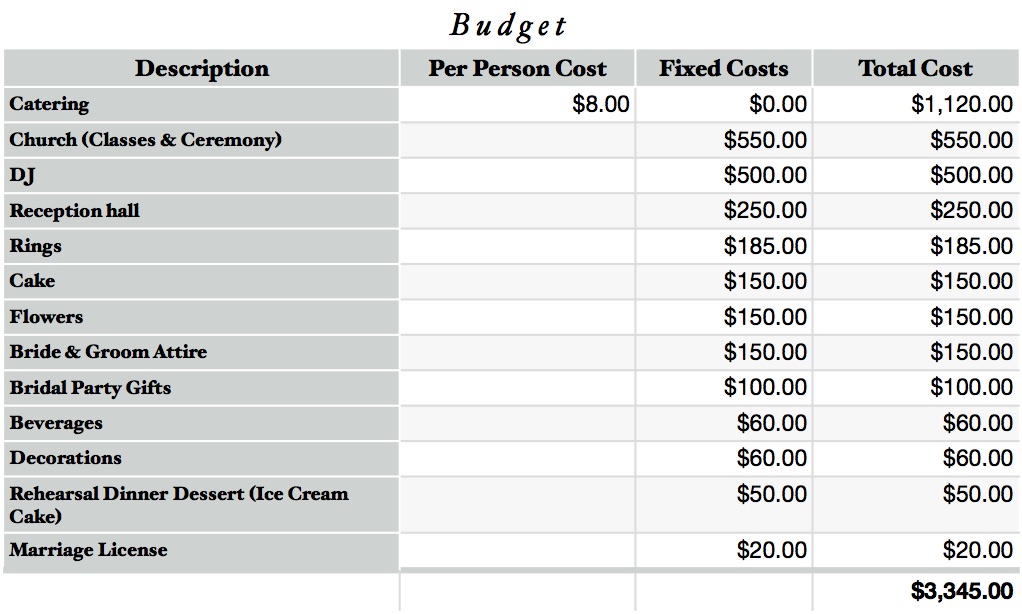

As you might expect, their wedding cost quite a bit less than the average $25k-$30k affair that most Americans have. Let’s take a peek at their budget.

Their biggest expense appears to be food and that was because they invited 110 guests to the wedding and had 30 for the rehearsal dinner. According to theKnot.com, the average wedding has 138 guests. Geez, if they didn’t invite so many friends and coworkers then they could have saved some money. Except they invited hardly any friends or coworkers. Almost all of the guests in attendance were extended family, and almost all of the guests at the rehearsal dinner were immediate family. Aye caramba!

$8/person is insanely cheap for catering. They scored a great deal by using a family friend who was just getting started in the business.

The menu was also very simple. Chicken, potatoes, corn on the cob, salad, and bread. The rehearsal dinner was beef brisket and switching the two or just doing the brisket both nights would be the only change they would make.

The wedding cake was a no thrills two tier plus sheet cake. It was nicely done by a family acquaintance and was delicious. There were no leftovers.

The venue for the ceremony, a church, had some stipulations that added to costs, such as required marital classes. At $5xx some dollars it wasn’t a budget buster.

One expense they could have cut would have been the DJ. Instead, spending more on alcohol would have helped guests have a better time. They scrooged on alcohol though because the reception venue said no (it was never enforced however).

Speaking of the reception, for a measly $250 they were able to use a community center for three days (rehearsal, reception, and brunch). That was a big money saver.

Their wedding bands were plain white gold bands from the department store.

The wedding photographer was Andrew’s brother and sister-in-law. The invites and RSVPs were designed and printed by another brother as wedding gifts.

Shae’s dress was a family heirloom. Some alterations were made for $50 and additional money was spent to clean and preserve it after the wedding. The headpiece was made by her mother.

In hindsight, things could have been done even cheaper. We went to a wedding last year that was very well done and almost certainly done on a smaller budget than ours. We did consider eloping, but figured our parents would kill us. Plus if we eloped we wouldn’t have funny photos like these:

Our honeymoon was a quiet week in the Midwest. The budget was around $1000 and included a hot air balloon ride (something that got rescheduled for our 1 year anniversary).

All told, wedding + honeymoon cost us $8,837.08 according to financial statements. Both were over budget due to all the nickels and dimes. With that said, I don’t think we would make too many changes from our younger counterparts. I for one am glad that we did not elope, as we often talked about when wedding planning was getting stressful. I am also glad that we abandoned the idea of having an outdoor reception on the family farm. Not only would it have cost more, but the stress of it possibly raining would have put everyone on edge. Especially when the morning sky looked like this.

At the end of the day, whether we had a big wedding or a small wedding. An expensive one or a frugal one, the thing that matters is the marriage. Mawage. Mawage is wot bwings us togeder tooday (for all of you Princess Bride fans).

It’s time to get back into the time machine and come back to the present.

The weather has been quite frigid the past few days, and that has forced us to stay indoors. Here are some of the activities we have been doing to keep ourselves entertained.

Free RedBox DVD Rentals

From now until January 18th, you can get free rentals by using code 45TH8787. Get one movie on day 1, return it the next day and use a different credit card to reuse the code on day 2. Rinse and repeat until you are out of card numbers.

Story Time at the Library

Our public library offers children’s story time every second Saturday of the month and select week nights. Bundle up junior and expose him/her to some culture. Frugal Boy was more interested in the audience than the guitar playing librarian.

Build a Fort

Use boxes, blankets, and furniture to make a fort in your living room. Have fun crawling through it, resting in it, and ultimately, destroying it.

Assemble Christmas Gifts

If you haven’t already, go ahead and assemble some of the Christmas gifts and take them for a spin.

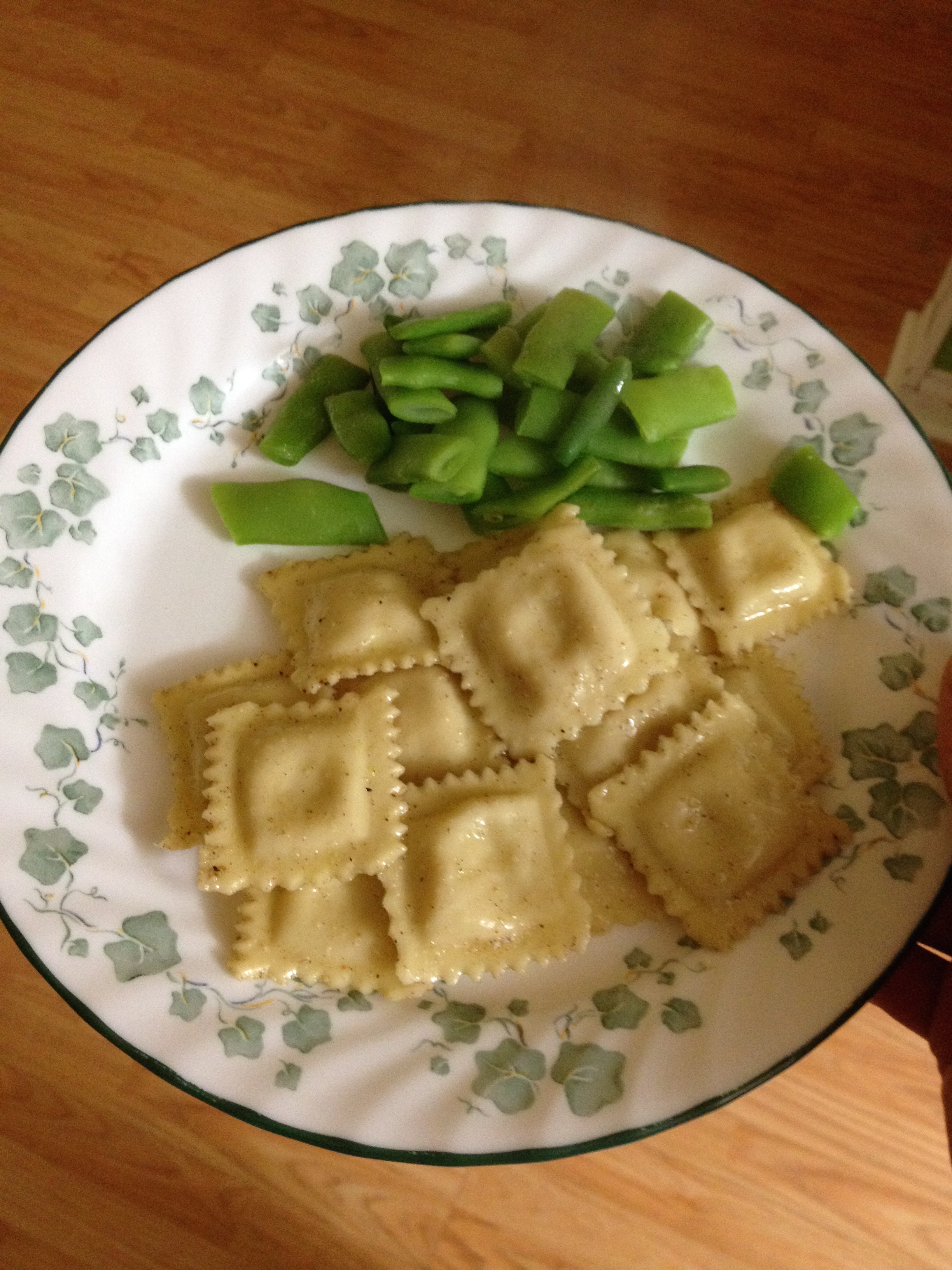

Cook a Fancy Dinner

We made four batches of homemade gorgonzola butternut squash ravioli. Our local high end Italian restaurant serves it for $14/plate. We made it for about $2/plate.

Blend together your filling.

8 oz gorgonzola to 3 lbs roasted butternut squash

Then prepare your dough.

1 egg to 1 cup all purpose flour

Blend and add enough water so it will stick together when you squeeze it.

Knead the dough into sheets.

Keep kneading until the desired thickness is achieved.

Switch to your ravioli maker.

Add the filling.

Crank out beautiful ravioli!

Every 1 cup flour/1 egg will make one sheet of ravioli.

Freeze some for later.

Cook and eat the rest!

What are you doing to stave off cabin fever on these cold winter days?

With the first year of 529 contributions under our belt, it was high time to take a look back and see how they did. The first thing I did was log into the online account and see the rate of return posted in big bold letters.

3.4%

Wow, that is terrible, especially considering that the fund we invested in returned a healthy 9.9% in 2014. Obviously something else is going on and you may have already guessed it.

That’s right, we didn’t invest everything on January 1st, instead we made contributions throughout the year. By giving Frugal Boy a big Christmas present/contribution, it effectively killed our rate of return because of the sudden influx of fresh cash that diluted previous gains. To properly calculate your return, weighted for irregular contributions, you will need to open up Microsoft Excel and use the XIRR function.

Here’s how to use the XIRR function.

In column A, enter positive contributions and negative withdrawals (or fees). In column B, use the Date function to enter in the date of that contribution. At the end of each column, enter the ending balance and date. Multiply your ending balance by (-1). So a positive ending balance would be displayed as negative (it’s just how the XIRR function works).

Finally, use XIRR(colA, colB, guess) where guess is your expected percentage return (e.g. 8%).

Here is an example:

Properly weighted, Frugal Boy’s 529 had a rate of return of 10.33%. Not too shabby 😀

Like our taxable investment account, we selected a low cost indexed fund that consists of:

70% VIIIX – Vanguard Institutional Index Fund

20% VDMIX – Vanguard Developed Markets Index Fund

10% VEXMX – Vanguard Extended Market Index Fund

The heavy equity exposure and associated risk seems appropriate for his age.

Today we simplified our investments. You may remember that we were contemplating making this move a while back (see here), but due to capital gains and taxes we had to wait until 2015 to avoid getting hit with a big tax bill.

Recap

We have condensed our portfolio from 6 mutual funds and an individual stock to a single mutual fund, Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX). This switch will give us broader diversification, VTSAX holds every publicly traded stock in America, and it lowers our expense ratio. The new lower expense ratio of 0.05% means that if you hold $10k for a year, Vanguard only skims off $5 to keep the lights on over in Valley Forge (their headquarters). Can you imagine walking up to a stock broker and saying “Hey buddy, I’ll give you $5 to invest my money in every company in the United States”.

Investing Made Simple

We’re not trailblazers by any means. You can read more about this strategy in more depth on other blogs.

I love the simplicity of the whole deal. Set up an automatic monthly investment and walk away. There is zero mental load associated with this plan. In fact, the less you think about it and worry about the market ups and downs the better. Fidgeting around with it is the biggest risk of losing money. So if you have 20+ years to kill time with and want to be set for retirement, consider setting up a lazy one fund portfolio.

Yesterday we did some Spring cleaning. If I call it that, will it make it Spring? Living with 24 pounds of curiosity is a great motivator to declutter and clean.

Yesterday we did some Spring cleaning. If I call it that, will it make it Spring? Living with 24 pounds of curiosity is a great motivator to declutter and clean.