Every year it is fun to look back and see the bird’s eye view of the past financial year. Mint.com makes that especially easy to do.

Our spending was heavily weighted by the down payment for an apartment building.

Spending by Category

Taxes normally dominates our spending followed closely by Kids (aka childcare). This year Travel made a big splash because we took two international trips. You can read about those trips here and here.

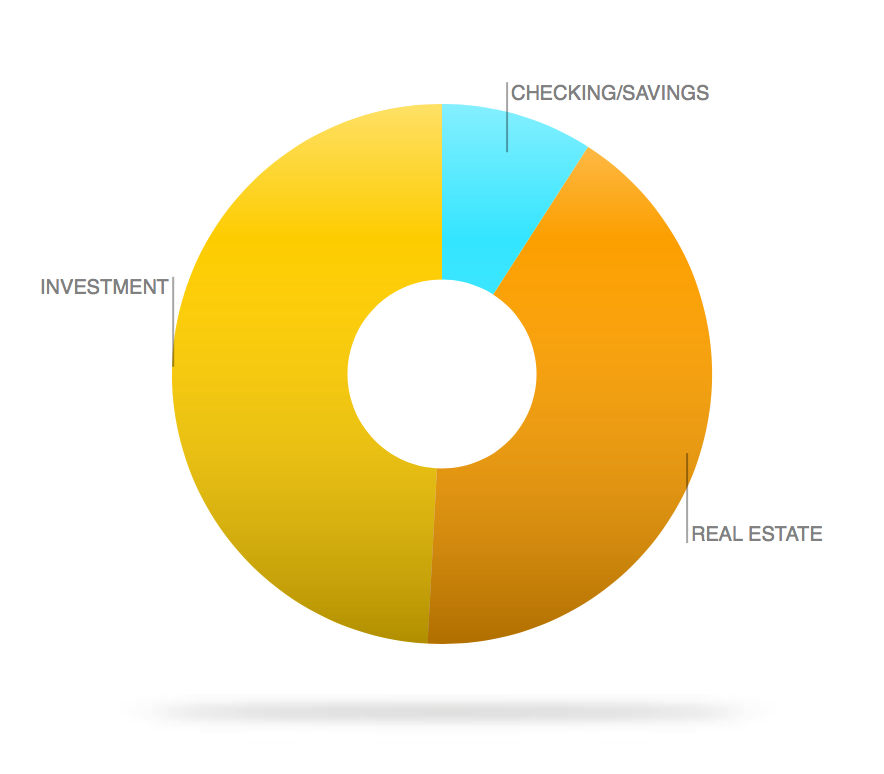

Our asset allocation has also shifted quite a bit over the past year. Our primary residence and apartment building now make up a significant portion of our assets.

Assets by Account Type

We still have the majority of our assets invested in the stock market under tax advantaged accounts (401ks, IRAs, 529s). We also have maintained a healthy liquid cushion should life throw us any curve balls.

The apartment acquisition also put us back into the debt game.

Debt By Type

Credit cards balances are still being paid in full every month, but the ‘Loan’ is the mortgage for the apartment building. At 3.5% for 30 years, I would consider it ‘good’ debt. We currently have no plans to make any accelerated payments.

Overall net worth (assets – liabilities) trended upward for 2016.

net worth (primary residence not included)

The upwards trend is a good sign that we are living below our means.

In some sillier number comparisons,

we used more water this year than in 2015. There are likely two reasons for this: 1. Frugal Boy is using more water than when he was a baby and 2. I replaced a super low flow shower head with a medium flow head.

~ 600 cubic feet more water used

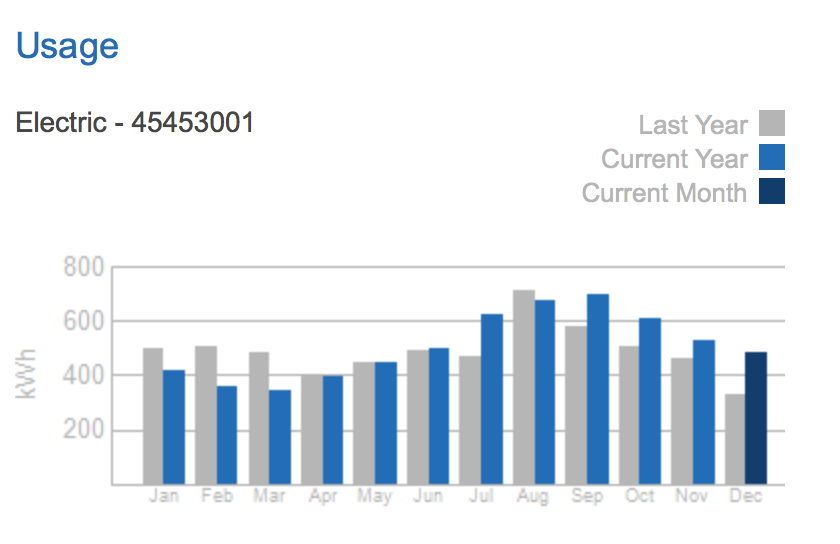

Electric usage is also up this year. There are more gadgets and gizmos in our house. I also ran power tools quite a bit this Fall while working on the basement remodel.

electric usage

Natural gas usage has remained inline with previous years. Insulation efforts have not yielded any major changes in efficiency.

natural gas usage

We used approximately 1.3 TB of internet bandwidth this year.

The weather has been frightfully cold. I know because I spent 20 minutes changing a flat tire this morning in a parking lot. Before you travel for Christmas or New Years, double check that your spare tire is in good shape, a jack, and tire iron are included and in working order. It is also a good idea to have a blanket in the car.

On a different topic, Shae and I enjoyed watching the movie The Company Men, starring Ben Affleck and Tommy Lee Jones. The movie follows several white collar workers who face downsizing during the 2008 financial crisis. It offers a great cautionary tale of living above one’s means.

Finally, after three and a half years, we have furnished all three bedrooms in our house with mattress sets and frames. The last acquisition was a $85 Craigslist bed frame made by the now defunct Cochrane furniture company.

If you live in the Midwest, you probably already know about the home improvement store Menards and their fantastic 11% rebate sales. What you may not know, is that Home Depot has a double secret probation rebate match program.

https://www.homedepotrebates.com/11percentmatch/

Whenever Menards is running an 11% rebate sale, Home Depot also runs a corresponding “Rebate Match” sale. The only difference is that Home Depot does not advertise it in any way that I’ve seen.

This is the first time that I am trying to take advantage of the secret match program. Hopefully my submission results in success. I have read on various forums that Home Depot does limit this to areas where Menards exists, so if you aren’t in the Midwest you might still be screwed.

Shae and I hosted Thanksgiving this year and my parents handed me an envelope filled with banking receipts covering years of my childhood. It could have just as easily been shredded, but since I have it, I might as well delve in and examine some of the financial going ons of my childhood. I have vague recollections of particular financial events, such as diligently depositing birthday and Christmas gift money, but now I have the receipts to piece it all together.

Then

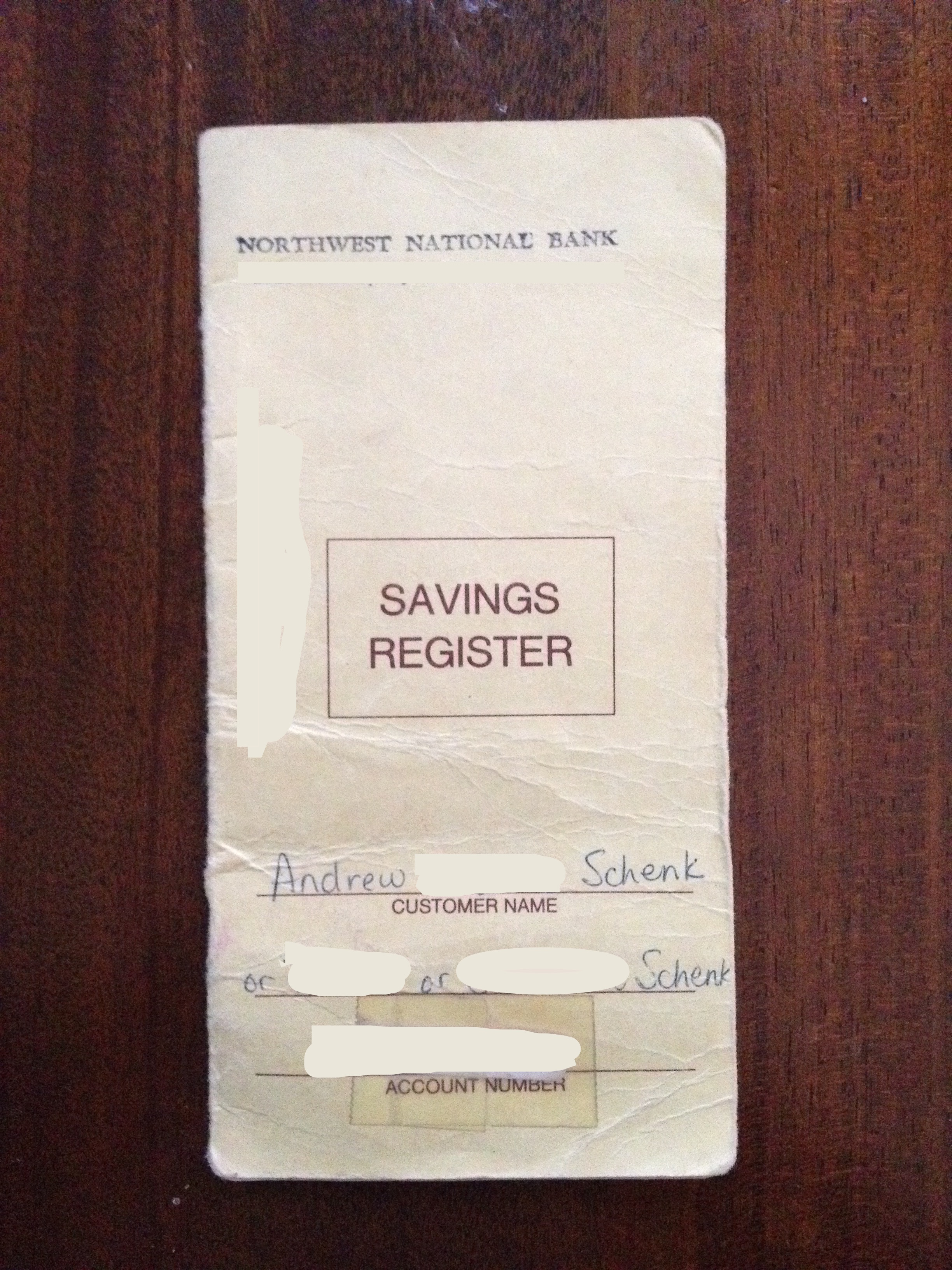

It all started when I was 3 months old. My parents opened up my first bank account. Gee, thanks Mom and Dad. Back in the olden days, there was no online banking. So I had a Savings Register to record transactions in.

Opening up the register, you can see the first deposit, and subsequently, how old I am.

That $310.00 adjusted for inflation would be equivalent to $660 in 2016. Thanks Grandparents, uncles, aunts, and family friends for pitching in for my financial future.

Over the years, the balance steadily grew. I particularly like the 4th or 5th grade me that deposited $25 of ‘prize money’ in 1998.

I have no memory of what contest I won back then, but an interesting thing begins to happen around that time period. The handwriting changes, and some of the entries are being made by a little boy.

Around junior high school, middle school, or whatever you call 6th, 7th, and 8th grades, I had saved up enough money, at my parents behest, to start meeting the minimum requirements of Certificates of Deposits, or CDs for short. I do remember my Dad always shopping around the 4 or 5 banks in town looking for the best CD rates. I also remember him on a trip up to Grandma Schenk’s house once bemoaning the fact that she did not shop around rates and was leaving money on the table by being loyal to the same bank forever.

Anyway, in ’00, there is a receipt of a CD being closed.

At age 13, the saver mentality had been thoroughly beaten into my head by my parents and I had approximately $3,000 to my name, the bulk of which was tied up in a CD.

Birthday’s and Christmas’s kept rolling by year after year, and year after year I would write a fistful of thank you notes to grandparents, uncles, and aunts before dutifully marching down to the local bank and depositing checks and cash. At some point my Dad made me go alone and stopped helping me fill out the deposit slips. Of course I was terrified, but it was a good sink or swim lesson.

My Dad kept optimizing the best savings rates for me and kept the bulk of my savings locked up in CDs.

This particular CD was kept open for 2 years before being closed. The grand total of interest earned over that two years was $231.47.

In 2004, I began working and earning money for myself. The pay was negligible, but the real payoff was learning the value of a dollar. Performing a mind numbingly boring task for hours on end to collect a small paycheck gives one plenty of time to think. Suddenly, that new flashy item being marketed to you seems a little less interesting when you replace the dollar cost with an hour cost. Something that costs $50, is the same as something that costs almost 10 hours of work for someone on Indiana’s minimum wage of $5.15/hr. Yes, that was what I started at. Spending several hundred of my own dollars to take a girl to high school prom did not seem like a balanced equation. A couple of hours of fun was not worth the 50 hours of work required.

Finally in ’06 as a senior in high school, I opened up my first solo bank account. I was now 100% in charge or my own finances. The rest as they say is history.

Now

Now the tables have turned. I am in the role of Dad, and Frugal Boy and Frugal Fetus are in the role of child. Just like my parents handled all the finances when I was born and slowly relegated duties to me over the years, Shae and I are doing the same with our children. Frugal Fetus doesn’t know it, but he/she already has a college savings plan opened up and partially funded. In fact, since it was opened in July, it has returned 6.83% APY. Frugal Boy’s 529 college savings plan has returned 8.95% APY for the year-to-date. On a more concrete level, any cash that Frugal Boy receives he diligently stores in his doggy bank at his parents behest. Any checks are invested into his college savings. Amusingly enough, Frugal Boy already recognizes and calls out the different bank branches as we travel through town. I think he is almost ready to graduate to his first real bank account. We will probably open a PNC ‘S’ is for Savings account for him. It has 0 fees for age 18 and under account holders and uses Sesame Street characters to encourage kids to save.

There are a number of savings programs available for kids. Here is a roundup of some of the more popular ones.

You may have heard of Moore’s law, in simple terms it was an observation made 50 years ago that computers would become twice as fast every two years. For the most part, this ‘law’ held true for the past fifty years thanks to scientific and manufacturing advances in semiconductor technology. Companies such as IBM and Intel were able to cram more transistors onto a silicon wafer by shrinking down the transistor size.

Over the past few years, Moore’s Law has been proclaimed dead or failed a dozen times by pundits. The real laws of physics seem to have caught up with transistors and they simply cannot be shrunk down any further before the electrons traveling inside start to do funny things, like teleporting. The result is a stagnation in computer CPU performance.

For example, consider the 2010 Macbook and its 2016 descendent. According to benchmark tests, the 2010 laptop scores 1536. By Moore’s Law, every two years, that score should double. You’d expect the 2016 to score 12,288, but it actually only scores 3221. So a six year difference only amounts to a doubling in CPU performance.

So why would you bother buying a brand new laptop if it is not leaps and bounds faster than a six year old machine? Well, typically because other components are leaps and bounds better. The two biggest areas are in Random Access Memory, RAM, and storage space, i.e. hard drives. Usually, both of these items are user upgradeable, so you can take that six year old machine and make it very competitive with a brand new machine.

The 2010 Macbook comes with 2 GB (gigabytes) of RAM, and a 250 GB spinning disk hard drive. For $100, you can upgrade that to 8 GB of RAM and a 250 GB solid state hard drive (SSD). A solid state hard drive is faster, lighter, and more robust than the traditional spinning platter hard drives of old. The computer will boot up faster, apps will start quicker, and the whole feel of the computer will be ‘snappier’.

Doing these upgrades on a 2010 Macbook is extremely simple. Use a philips screwdriver to undo the bottom cover screws.

You can see the blue RAM chips in the right side of the picture. The silver hard drive is in the bottom right corner.

The two RAM chips will pop right out from the motherboard. The hard drive has a couple additional screws holding it in place. Installation is the reverse.

After replacing RAM, it is generally a good idea to run a test. MemTest86 is a free piece of software that will do an exhaustive battery of tests. The setup instructions are a little technical, but once you have made up the flash drive or CD, the test itself is incredibly easy to run.

TADA! You now have a cheap laptop that is almost as good as a brand new expensive one. What a great deal for an ‘obsolete‘ machine.