Our 2015 property tax bill is now viewable online. We should be getting a paper copy in a few days. It is interesting because we are in almost a polar opposite of my parents. They have a very high county income tax, but pay almost nothing in property taxes. We have no county income tax, but extremely high property taxes (along with a flat state income tax and high sales taxes).

Public schools aren’t cheap. There is no such thing as a free education.

Frugal Boy got a doggy bank for Easter and he loves to put money into it. He even has a couple of dollar bills from a card given to him.

I am pretty sure that he doesn’t understand money, or the fact that it can be traded for more practical 2 year old things. If he did understand, he’d probably be trying to get that deposited money back out, but that is a lesson for another day. Right now, Shae and I are content to start building a habit of putting money in a ‘safe’ place.

Another life skill that we have been working on is grocery shopping.

He is good at not running into things or people, but we are still working on the concept of “Yours and Not Yours” or “The Stores vs Ours”. Those red grapes are awfully tempting, and he would frequently try to dash up and grab a couple while we were busy. He also thought that a gallon of not-butter should be placed in the cart, along with a carton of eggs.

Yesterday we went to the Peoria Zoo, Riverfront Museum, and Children’s Playhouse. All of the Peoria museums were having a membership swap day, so it was free admittance if you had a membership at any of them. We used our Prairie Wildlife memberships to gain access.

It was a cold day and the indoor places were packed with people. So instead of eating shoulder to shoulder with the crowds we employed a travel trick and went where the people weren’t.

Packing a picnic lunch is always a good life skill to learn.

Speaking of food, Frugal Boy has started to associate running with a good thing. About a month ago, when his aunt visited, Shae and I took our morning run with the jogging stroller as an opportunity to get donuts from our local bakery. Ever since then, Frugal Boy asks for donuts when we go on our morning run. We indulged him again yesterday. Hopefully exercise is now permanently associated with good things.

What if I told you that you could make your own FDIC insured certificate of deposit, that had the following terms:

3 month duration

5.4% rate

$15,000 minimum (anything greater than 15k will not earn interest)

FDIC insured

Does it sound too good to be true? Good news, it is true. Granted this is a Do-It-Yourself package, so it lacks the convenience of ‘official’ deals.

Here is the quick and dirty on how to make up this ‘CD’ for yourself. Note: You will need a local Chase bank branch in order to complete this.

Step 1

Obtain one of these Chase coupons. They can often be found in the junk snail mail, your email inbox, or in a pinch eBay.

Step 2

Open a Chase savings account in branch and fund it with $15,000 of new money.

Step 3

After the $200 bonus (aka “interest”) posts, withdrawal $14,900 to your regular accounts.

Step 4

After 6 months has passed from account opening, withdrawal the remaining $300 and close the account. The final $300 keeps monthly fees at 0.

Step 5

Profit! Congratulations, you made your own 3 month ‘CD’ with a rate far better than anything that you would find in pre-packaged deals. If you have a spouse, you could effectively turn this into a 6 month CD by shuffling the original seed money around accounts. A quick internet search showed that the best official CD rate for a 3 month term is 0.83%.

All of the fine print is below:

Chase SavingsSM has no Monthly Service Fee when you do at least one of the following each statement period: Option #1: Keep a minimum daily balance of $300 or more in your savings account; OR, Option #2: Have at least one repeating automatic transfer of $25 or more from your Chase personal checking account (available only through Chase OnlineSM Banking); OR, Option #3: Have a linked Chase Premier Plus CheckingSM, Chase Premier Platinum CheckingSM, or Chase Private Client CheckingSM account. Otherwise a $5 Monthly Service Fee will apply. A $5 Savings Withdrawal Limit Fee will apply for each withdrawal or transfer out of this account over six per monthly statement period.

To receive the $200 savings bonus: 1) Open a new Chase SavingsSM account, which is subject to approval; 2) Deposit a total of $15,000 or more in new money into the new savings account within 10 business days of account opening; AND 3) Maintain at least a $15,000 balance for 90 days from the date of deposit. The new money cannot be funds held by Chase or its affiliates. After you have completed all the above savings requirements, we’ll deposit the bonus in your new account within 10 business days. The Annual Percentage Yield (APY), for Chase SavingsSM effective as of 2/22/16, is 0.01% for all balances in all states. Interest rates are variable and subject to change. Additionally, fees may reduce earnings on the account. You can receive only one new checking and one savings account opening related bonus each calendar year and only one bonus per account. Bonuses are considered interest and will be reported on IRS Form 1099-INT.

**Account Closing: If either the checking or savings account is closed by the customer or Chase within six months after opening, we will deduct the bonus amount for that account at closing.

The Employee Benefit Research Institute, or EBRI for short, just released their 2016 survey results of 1000 workers and 500 retirees. The annual survey has been ongoing for a couple of decades now, so it provides a good indicator of where Americans are in regards to retirement confidence and thought process.

You can view the full survey brief here: https://www.ebri.org

My own conclusions after skimming through the charts and figures is that Americans are still on course for a rude retirement awakening.

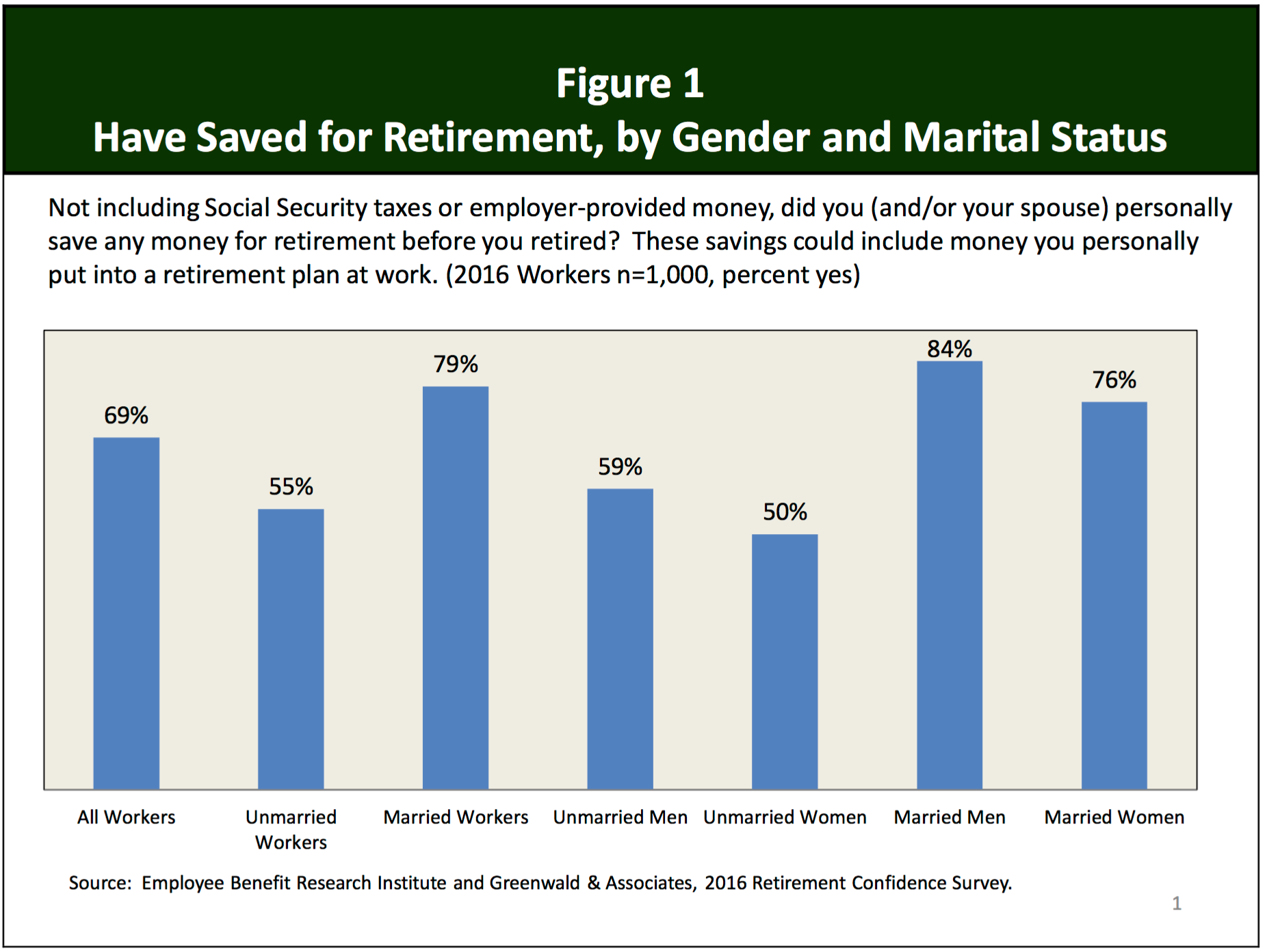

21% of workers in 2016 are confident that they will be able to retire comfortably and 19% are not at all confident with the rest in-between, but 67% of current workers expect to continue working in retirement.

Compare the blue line (current workers) with the red line (current retirees). Either we are going to get used to seeing older people in the workforce, or a lot of people are going to be in for a rude surprise when they cannot find employment as they get older.

Looking at the Savings and Investments by age doesn’t exactly inspire confidence. The Baby Boomer generation is woefully underprepared for retirement with 1/3 of respondents claiming less than $25k in savings. That would probably cover 1-2 years of living expenses. Gen X and Y (Millenials) aren’t doing much better.

Married men seem to be the most motivated to save for retirement. Unmarried women don’t seem to have the same kick in the pants.

A whopping 23% have raided their retirement accounts for present day needs/wants.

I think the biggest threat to retirement in America is people simply burying their heads in the sand. They know that it is a problem, but it is easier to kick the can down the road instead of dealing with it right now. The problem is that developing a solid retirement takes time! Kicking the can down the road isn’t the answer!

What can be done to help avert a retirement crisis? Enroll in your employers 401k plan and/or setup an IRA. Workers enrolled in a plan had significantly more saved than workers not enrolled. Paying yourself first works!

It has been a little under 2 months from our first churning credit card application (read more about that here). In case you have no idea what I am talking about, credit card churning is the process of signing up for credit cards with the sole goal of collecting hefty signup bonuses from the bank. We have a trip planned for Costa Rica this summer and we wanted to see just how much money we could knock off the total bill.

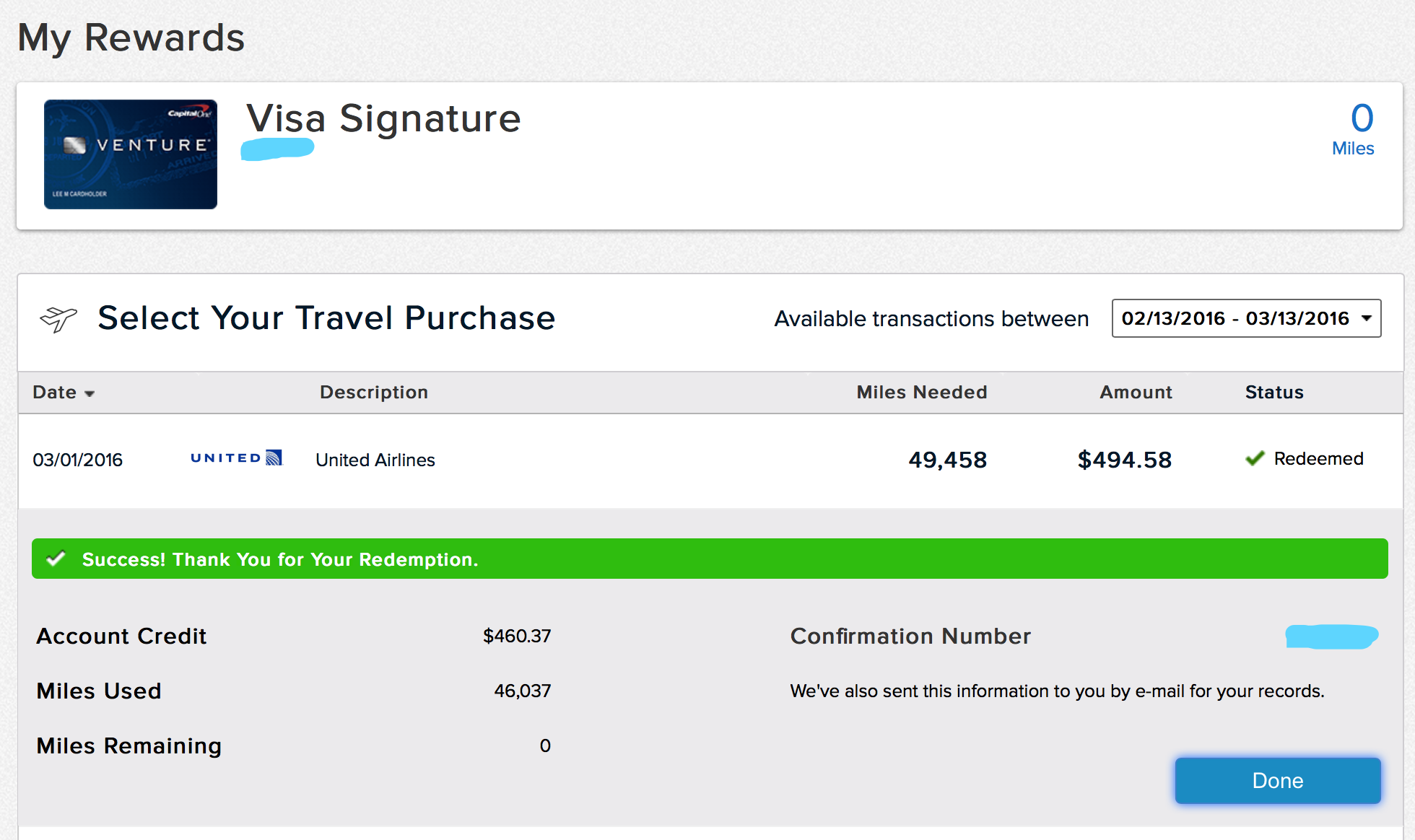

The first credit card that I targeted was the Capital One Venture card. I just completed the requirements to get the bonus for that card and the 40,000 bonus points posted soon after.

I was able to redeem the full point total against a plane ticket to Costa Rica to knock $460.37 off a $494.58 ticket. 93% off airfare isn’t too shabby!

Shae also got into the game and completed the requirements for the Barclaycard Arrival Plus. When we purchased airfare, we did it in two separate transactions so that we would be able to redeem multiple credit card bonuses against the cost.

Barclaycard Arrival + is a very similar setup to the Capital One Venture card. 40,000 bonus points are awarded for spending $3k in 3 months. One of the small differences between the two is that the BA+ card can only be redeemed in increments of 2500 points. Shae was able to get $450 applied towards a $494.58 airfare.

I am quite pleased that with two cards we were able to save $910.37 in travel expenses. That will go a long way to reducing the cost of our Costa Rica trip this summer.

But Wait, There’s More!

I’ll admit it. I got hooked. Credit card churning has been an enjoyable distraction for me. If you read the fine print, have clear goals, and a modicum of self discipline you can rack up quite a bit of ‘free’ money.

My spreadsheet has grown considerably from that initial blog post two months ago. Yes, it is color coded now according to the card issuer. Click on the image below to see a bigger more readable version.

In total we have applied for 8 cards.

Chase Freedom

Annual Fee: $0

Bonus: $150 + $50 for referer

Min Spend: $500

Min Spend Deadline: 3 months

I already have this card and it is one that I use on a monthly basis. Chase keeps sending me emails to pimp this card out to my friends and family. If someone signs up for the card through my referral link, I get $50. No, I won’t put the link on this blog.

Shae signed up through the link however so this card should net us an easy $200 and because it has no annual fee, she can hold onto it forever.

BankAmericard Travel Rewards

Annual Fee: $0

Bonus: $200 statement credit

Min Spend: $1000

Min Spend Deadline: 3 months

Both Shae and I applied for this card. Shae was approved and I was denied. Ironically, because I didn’t have enough credit card accounts. Hehehe. The plan is to use the card and bonus for Costa Rica lodging.

Chase Sapphire Preferred

Annual Fee: $89, waived first year

Bonus: 55000 Ultimate Reward Points (between $550 and $687)

Min Spend: $4000

Min Spend Deadline: 3 months

I got this card for future travel. We plan to meet the min spend by paying our property taxes with it. Yes, our property taxes are almost $4000/year. We might as well get a bonus while we rip off the tape.

IHG Rewards Club

Annual Fee: $49, waived first year

Bonus: 60,000 points + $50 statement credit OR 80,000 points

Min Spend: $1000

Min Spend Deadline: 3 months

I got this hotel credit card because it is a surprisingly good value. In addition to the one time bonus, you also get a free night every year starting on your second year of membership. Essentially, you get a $49 night at any IHG hotel. The lower tier hotels start free nights at 5-10k points. 80k reward points would be enough for around 8 free nights. If you figure those are $80 nights normally, then the bonus is worth around $640.

Chase Total Checking

Monthly Fee: $12 unless criteria are met

Bonus: $300

Bonus Requirement: Make a direct deposit of at least $500.

Bonus Req Deadline: 2 months

This one isn’t a credit card! It is a checking account. The $300 bonus was a targeted offer that Chase sent me. They really want me to be a customer, so they offered a big bonus to lure me in. The requirements are pretty easy to meet. Open it up in branch with the targeted coupon code, dump $1500 in to satisfy the monthly fee requirements, and then make a direct deposit of $500. Wait 6 months to satisfy the fine print and then close the account. Abbra Cadabra, $300 for about 3 hours of work.

Wrapping Up

All told we are looking at about $3200 in bonus churning provided that we meet the various requirements and are able to optimize the bonus redemptions. I like that I can do most of this from my computer and it doesn’t hurt that we can stick it to big companies in the process.

Speaking of Which

Did you see the credit limits that we were approved for?! Holy crap. No wonder why Americans are in debt up to their eyeballs. It is so easy to get ridiculously high credit lines. Why in the world do credit card companies think that handing out $127,900 of available credit to a couple of twenty year olds is a good idea. The morbid reason is simple, the companies are hoping we self destruct and spend more than we can pay off. If we fell into that trap, then the companies make money in insanely high APRs ranging from 14% all the way up to 22%. These companies want people to pay the minimum. So sure, give Andrew a credit limit of $25,000 and hope he screws up and becomes a wage slave. That is why I have zero empathy and zero remorse from milking these card issuers for big bonuses. I’ll play the game, but I’ll play it on my terms.