Last night I watched a great little documentary by PBS Frontline about the shift in retirement responsibility. The documentary, available online for free viewing, provides a short history of the pension to 401k historical shift, follows some regular Joes and Janes, and interviews several major executives on Wall Street.

The easy to digest one hour long video does a great job exposing the hidden cost of expense ratios in certain 401k plans. Two next door neighbors working the same job and contributing the same amount can have drastically different retirement savings because of these often overlooked fees. In fact, the example given by Vanguard founder John Bogle, was almost 2/3 less savings due to high fees.

The documentary fell a bit short in highlighting successful savers who have navigated the somewhat murky waters of retirement savings. Not all 401k plans or choices are bad, and not all pensions were/are good. It is undeniable though that in this day and age, the responsibility for saving and preparing for retirement is ours, not our employers.

Shae and I have kicked around the idea of buying investment real estate for several years. Today, we finally pulled the trigger. In all truthfulness, the moment came several months ago when we submitted a bid on an apartment building. It has just taken until today to finalize all of the legalese. Buying real estate isn’t for the faint of heart!

So what is so special about real estate as an investment tool. In one simple word, ‘leverage’. Putting someone else’s money to work for yourself is relatively easy in the world of real estate. Mortgages are advertised by virtually every bank, credit union, and even insurance salesmen! Right now, we are living in an almost unprecedented environment of cheap borrowing. The prime mortgage rate for a 30 year fixed rate loan is hovering around 3.5%. In fact, that is the rate we secured. I remember when I was a kid and you could have a savings account earn more than that.

We have talked together for years about what type of property we would want, why that would best achieve our goals, and how we would want to operate it. For us, residential housing, aka apartments, with a buy and hold strategy was a natural fit. Earlier this year, we got serious again about getting out of the armchair and into the field. We ran numbers on dozens of different properties for sale. I adapted a simple back-of-the-napkin model from BiggerPockets.com and used that to get a better idea of how different properties sized up to one another. Eventually, we started to get a feel for our local market. There were some abysmal numbers out there, a lot of mediocre ones, and some that seemed too good to be true. We started calling realtors and visiting places in person. Sometimes the numbers lined up with what we saw in person. For example, one place had an amazing rate of return on paper, but in person it was obvious that it was a high turnover, hard to collect rent type of place. When the tenants have smashed holes in the drywall, you run the other way as fast as your legs can carry you!

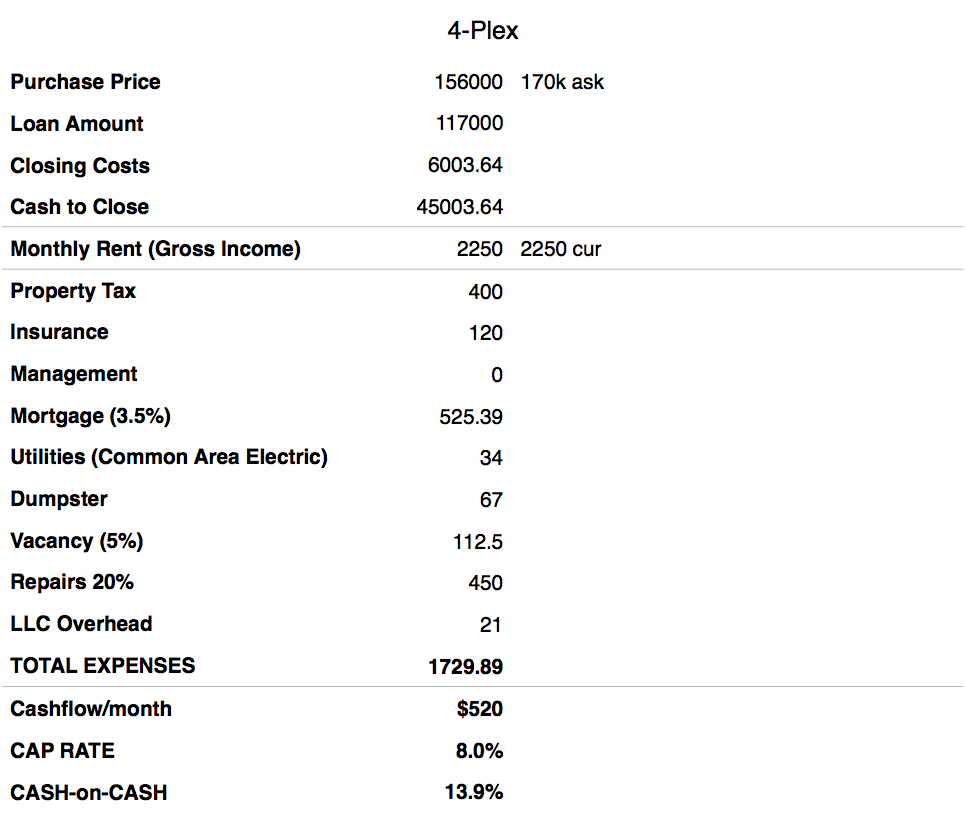

Eventually, we spotted an attractive looking quadplex that ticked off all our checkboxes. It had a simple geometry, was purpose built for apartments, good neighborhood, and was taken care of by a respectable owner. The ask price was 170k. We offered 151k. Other buyers put in bids, counteroffers ensued, and we eventually won with an offer of 156k. Below you can see our napkin investment math.

Monthly Rent through Total Expenses are on a monthly basis. The CAP RATE, or capitalization rate, would be the investments rate of return. Leverage is what makes the work worth it though. CASH-on-CASH is the rate of return that we are forecasting for the profit, cashflow/year divided by the cash to close. In essence, we made an investment of 45k dollars and expect to make 6k a year in profit. Of course, only time will tell how well it actually performs, but at some point you just have to jump in and start swimming. The other huge benefit of real estate is depreciation, but I’ll get into that closer to tax season.

This blog is about being frugal, and one of the advantages of being frugal is that you might be able to retire earlier or retire on less than the ‘norm’.

One of the internet forums that I peruse on occasion is reddit.com/r/financialindependence the community is full of individuals and couples that are looking to retire securely and possibly even decades earlier than the conventional 65-67.

This summer, there was an open survey on that forum, that asked participants a variety of questions concerning their personal finances. Just recently, the results of that survey have been posted. With over 1300 responses, there are some interesting conclusions that can be drawn, but I just want to focus on one.

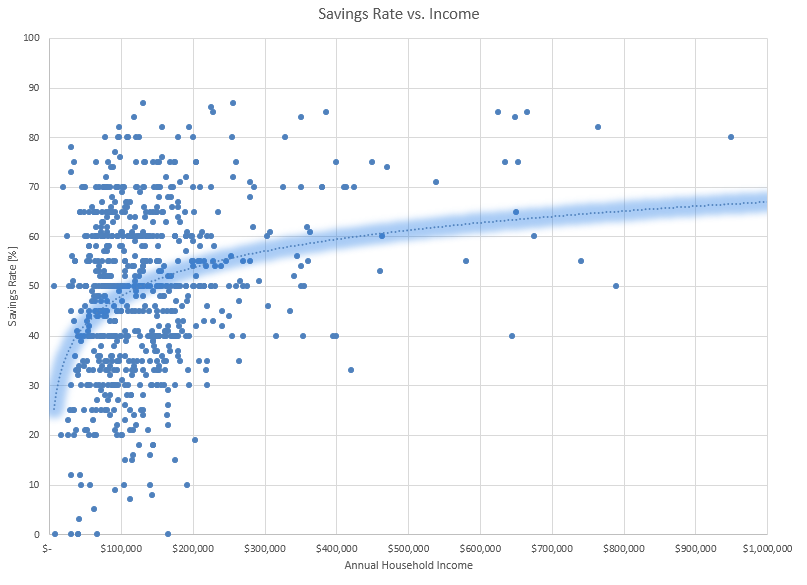

Savings Rate vs Income

We all know what income is, for example if you earn $40k/yr and your spouse earns $20k/yr and you have no other sources of income then your gross income number would be 40k + 20k = $60k/yr. Savings rate, is the percentage of that gross income that is left over after all of your yearly expenses, taxes, healthcare, etc are deducted from your gross income. In the above example, if you have $10k left over at the end of the year then your savings rate would be 16.6%. As a reference, Vanguard recommends that households put away 12-15% of their gross income away for retirement each year.

The forum members on financialindependence are not representative of the general population. Most of them are SINKs or DINKs (Single Income No Kids or Double Income No Kids) living in HCOL (high cost of living) areas such as the East or West coast cities. Usually, they have very high incomes that are multiples of the median US household income, $52k/yr.

With all of that said, you would think that the higher the income became, the higher the savings rate would be. After all, if you made one million dollars a year, surely you could stash away 90% of that. Couldn’t you?

It turns out, the data says something different. While savings rate does trend upwards, it is a very, very weak pattern.

Households making $100k/yr, nearly double that of the median household income in the US, are stashing away about 50% of that (keep in mind these are for people pursuing early retirement). Now look at the households making twice that, $200k/yr. The savings rate is still around 55%, a mere 5% increase despite a 100% increase in income.

What Gives?

There could be any number of reasons.

Higher income households may have more student loan debt (doctors, lawyers, etc)

Higher income households have a higher tax burden (28%+)

Higher income households could be located in higher cost of living areas (NYC, San Francisco, D.C.)

There could be a psychological barrier (I earned it, I deserve something nice)

I am not sure what exactly is going on behind the numbers, but I find it fascinating regardless.

What About the 1 Percenters?

If you widen out the chart to include truly preposterous incomes you’ll see two things happen.

There aren’t as many data points, so it becomes harder to identify trends

The existing trend doesn’t change much

Why Should I Care?

That’s a good question, and it has a simple answer. The time until you can retire doesn’t depend at all upon your income, it depends on your savings rate. The greater percentage of your income that you can save for retirement each year, the earlier you can retire. A popular early retirement blog explains the idea. For example, saving Vanguard’s recommended 15% of income each year equates to 43 working years. Saving 50% equates to 17 working years.

The question isn’t, “how can I earn more so I can retire faster” but instead, “how can I reduce my expenses and be more frugal so I can retire sooner?”

You can see some more of the survey results represented in purdy pictures here.

In the peaceful forest of Tuckville there was a mighty oak tree. Each year, all of the squirrels in the forest would work together to collect all of the acorns from the tree.

The youngest and smallest squirrels would gather acorns from the very top of the tree. The branches were itsy bitsy, but that did not scare Sammy.

Sammy ran along the branches to the very tippy end and would pick an acorn before racing back to the ground and adding it to the big pile of acorns.

When all of the acorns were harvested, the oldest squirrel would give each squirrel a share of the pile. The oldest and biggest squirrels who collected the most acorns, would get more, and the younger smaller squirrels like Sammy would get less.

Most of Sammy’s friends would eat their acorns right away. Some of them would trade their acorns for a car.

Sammy thought about what he wanted to do with his acorns and he got an idea. He took them down by the creek in a nice sunny area and he buried all of his acorns.

For the rest of the Fall, he watched as his friends raced around in their cars.

The next Spring, Sammy went back to the creek and saw dozens of little oak trees were he had buried his acorns.

10 years went by, and Sammy was no longer a little squirrel. He was a big adult squirrel. Back by the creek, it was no longer sunny. There were big oak trees there now, and they had huge amounts of acorns!

His friend’s cars had long since broken down. They had nothing left to show from their long days of picking acorns from the mighty oak tree, but Sammy had an entire grove of oak trees all to himself.

He picked all of the acorns from the trees that he had planted so long ago and traded those acorns for a nice house where he could raise his own family.

The End

So ends, my little parable. Isn’t it nice and cliche? Would you believe me if I said it was based on a true story? My story to be exact.

When I was in high school, I worked as a dish washer for the local college. Looking at my social security earning reports on SSA.gov, I made $1350, $1046, and $733 for the three years that I worked there. I remember that my wage was $5.35/hr and my sophomore year of high school, I worked during the school year as well as the summer.

Most of my friends also worked during high school, and some of them worked to drive. “I need the job, to afford the car, to get me to the job.” I rode a bike, and was fairly unpopular. Having a car is a big status symbol here in the Midwest. It is something of a rite of passage for teenagers. The sweet 16th birthday. Of course, $3k doesn’t buy a whole lot of car.

It did however buy around 50 shares of AAPL stock. A decade later, when I ‘harvested’ that initial investment, it had grown to the tune of around $30k.

I didn’t know it at the time, but I was the best paid dishwasher in that cafeteria making an adjusted $53 an hour. Perhaps if I had known, I might have been more tolerant of the infantile college students behavior of making toddler sized messes of their food trays.

So what happened to that windfall investment? Well, most of it went towards clearing up student loan debts from college, but the remainder became part of our down payment on our house. Who knew that cleaning dishes would be so enabling?

Obviously, there was a lot of luck involved with putting all of my acorns in one basket. What wasn’t lucky, was my decision to take the path less traveled and forego my teenage desires for mobility, freedom, and instant gratification.

I eventually did buy a car and a cellphone. It only took until I was a junior in college.

My employer announced changes to the paid time off (PTO) policy today. Though it’s being touted as “better” and “more in line with industry standard,” like most benefits changes it’s meant to help the employer not the employee.

The current system is set up such that for XX number of years of service you get XX days of personal vacation (renewed in June), XX days of personal sick leave (renewed on your anniversary), and 3 days of personal time (renewed every January). The rules for how you can use each vary. The new system will do away with that and combine everything into one bucket with some special rules for long term federally protected leaves and one-off events like jury duty and funerals. Instead of once a year allotments, employees will get a fraction of their PTO days every pay period. Less tenured employees who don’t use a lot of sick time, like myself, will see an bump up in usable PTO days. Pretty nice huh?

The extra days up front will be a boost in the short term but after you do the math anyone staying long term will lose out compared to today’s plan especially with the new accrual caps and timings.

It is always good to have a back up plan as employee benefits packages can change suddenly and without warning. Just a few years ago there was a radical change to the post-retirement healthcare subsidies that left many retirees and soon-to-be retirees confused as to what exactly was going to happen to their healthcare and how they could afford it. In the past you could put in 35+ years of service and retire with a guaranteed pension. That doesn’t happen much anymore. Employers have to change to stay solvent. I wouldn’t be surprised if our own pension and 401k plans were to change over the next decade given the aging workforce.

By taking responsibility for your own finances and not relying on anyone else to provide for you (whether that be your employer or the government’s Social Security) you cushion yourself from the sudden benefits changes that may devastate someone else. Our goal to be financially independent by 40 makes the new PTO policies an non-issue for us. We’ll happily take the extra days off that we would have had to wait years for. By the time that the new policy would become a negative we’ll hopefully be in a spot where we are a) completely retired b) cut back to part-time or c) selfishly employed somewhere else (in no particular order of preference).