I just submitted our Federal and State income taxes for 2015. The numbers were very similar to 2014. We had an effective tax rate of 11% with total income compensation that would place us in the 25% bracket.

This year, like previous years, we did our taxes ourself using pen and paper. Maybe sometime in the future we will switch over to an accountant or software, but our situation isn’t overly complicated (yet).

One W2

1040

Ordinary/Qualified dividends

Schedule C (business income)

Schedule SE (self employment tax)

Schedule D (capital gains tax)

Form 8949 (helper form for Schedule D)

I like doing taxes ourself because it forces us to learn about the tax code and helps identify what changes we can make to reduce how much we pay. Software tools such as Turbo Tax like to advertise guarantees for the best refund possible, but they don’t give advice on how to improve for next year.

For instance, this year I learned that we did not qualify for the dependent care benefit. I had written previously about using both a FSA, flexible spending account, and the DCB but it turns out that our FSA of $5000 disqualifies us from any DCB credit. What I did learn however is that it would work with 2 or more dependents. Tax software isn’t going to tell you that.

Our goal for 2016 is to dump as much money as possible into tax protected accounts. Taxes in general, but especially income taxes are our largest expense now that our house is paid off. In 2015, federal income tax, state income tax, property tax, and sales taxes took about a twenty thousand dollar bite out of our budget. Ya, I don’t like taxes.

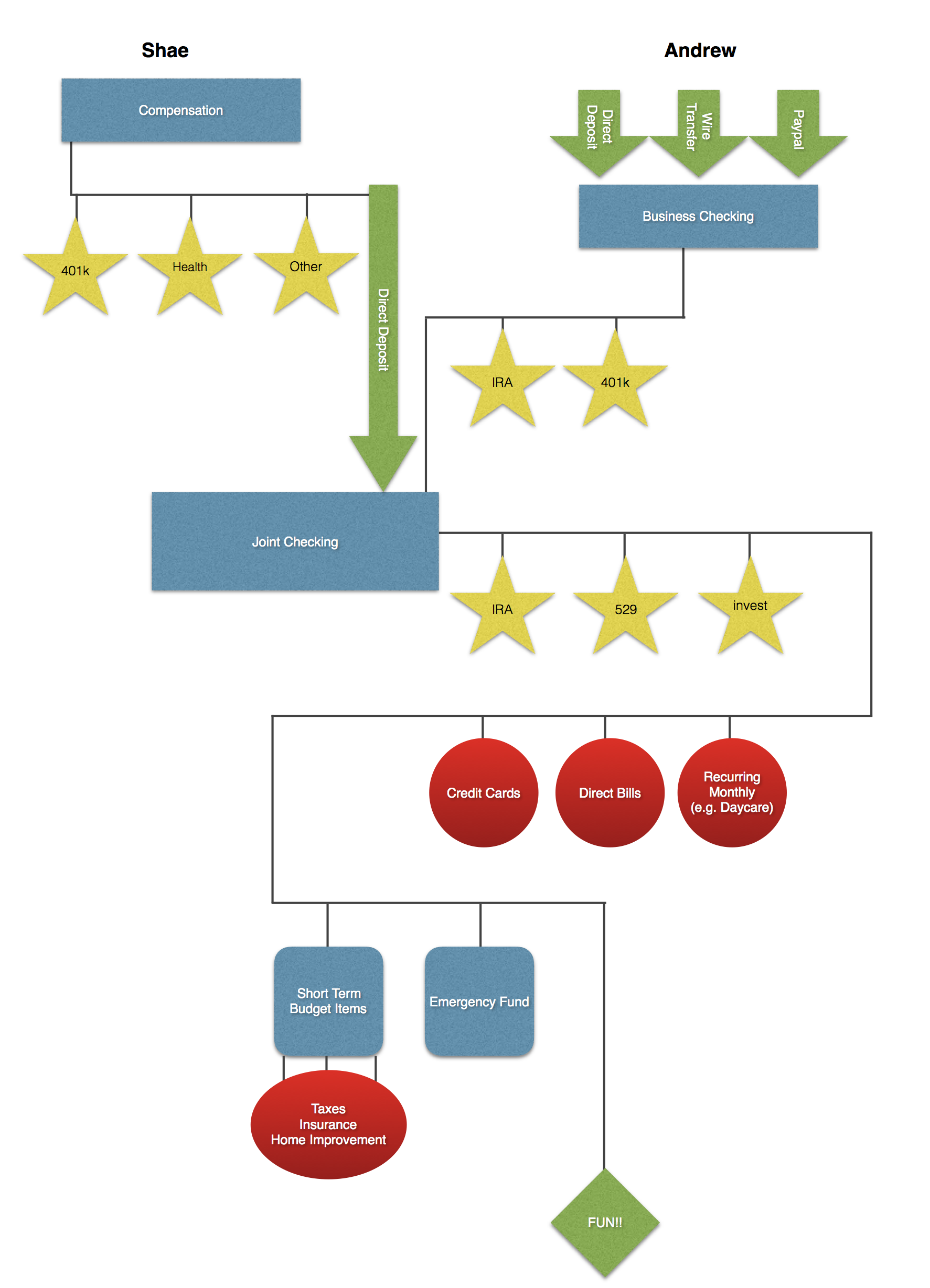

You have probably heard the saying “Pay Yourself First”. A few years ago, I saw a graphical representation of that saying that used water and buckets to represent the flow of money. In that analogy, income/money comes pouring down from the top and fills or leaks out of various buckets as it cascades down to the bottom. It is up to you to decide what buckets get filled up first and how much water is wasted (frivolous spending). Below is a rough representation of how money flows through our personal finances. You can see how we have put “paying ourselves first” as a top priority as those are the first buckets to be filled up.

If any water makes it to the bottom of the pipeline it can be used for FUN!!

Are you making the gold star buckets as big as possible? Have you reduced your red leaky buckets to the smallest they can be? Is your FUN!! at the end of the line, beginning, or somewhere in-between? Have you set up any reservoirs (emergency funds) for future droughts?

I have heard about credit card churning for several years now and it has never really interested me before. That began to change after our Mexico trip when the lights upstairs started to flicker on about ways to trim the fat on our next international trip.

What is Credit Card Churning?

Credit card churning is the act of signing up for credit cards for the sole purpose of collecting the, usually, large sign up bonus offer. As soon as one bonus is collected you move on to the next card. Some industrious, or foolhardy, individuals may open multiple cards at once to speed up the process.

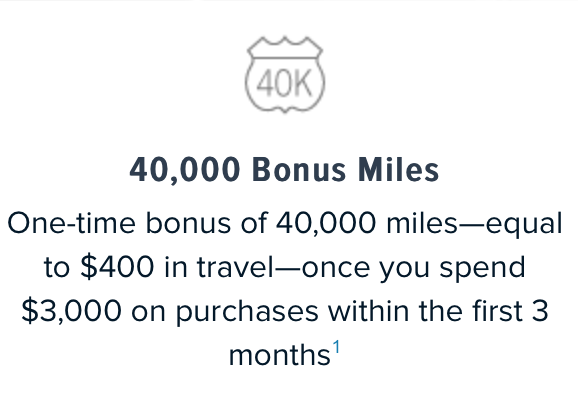

Example Sign up Bonus

Here is another example sign up bonus. This one from Capital One’s Venture card.

Why Bother?

If you do it right, and that is a very understated statement, you have a lot to gain and very little to lose. Take the Venture card for example. If both you and your spouse complete the necessary bonus steps, you stand to save $920 on travel. In the case of our Mexico trip, that would have nearly halved the trip cost!

What’s the Catch(es)?

Tons. We are talking about credit card companies who make money by taking advantage of uninformed or ill informed individuals. Here are just a few of the gotchas you have to consider.

Minimum Spending Requirement

In order to receive that big points bonus, you usually have to spend a certain amount with the card within a certain period of time from being approved. For Venture, that is $3k within 3 months of approval. If you only spend 2999, you are SOL. No bonus points for you. You might think, that will be a piece of cake. I’ll just go to the ATM and withdrawal three grand. WRONG! That counts as a cash advance and will generate 25% interest immediately. A big no-no. Serious churners who take out multiple cards at once often rely on manufactured spending, or MS for short. MS is the process of using the credit card to obtain some sort of cash equivalent and then figuring out a way to get that equivalent back into their bank account. There are many different strategies for doing this, and most of them are perfectly legal. The strategies are always changing however as loopholes are closed. I would strongly advise that you do plenty of research before going down this rabbit hole.

For myself, I am intending to avoid MS altogether and reach the minimum spending through normal usage. It is important to consider whether or not you can meet the minimum spending requirement.

Annual Fees

With high sign up bonuses, come high annual fees. The Venture card and several others, waive the fee for the first year. The card companies hope that you’ll like the card so much or just forget about it that they will be able to milk the AF for years to come. You’ll need to have an exit strategy to deal with the annual fee. Sometimes you can downgrade the card to a $0 AF, or you may have to cancel the card outright. All of this needs to be taken into consideration BEFORE applying.

Credit Score

Your credit score will take a hit from doing this. Churning is not recommended for anyone with low credit or anyone that may need credit for something important (like a house or student loan). I am in a nice position where my credit score doesn’t really matter because I don’t need it for anything vital.

Point Redemption

What are you going to spend those bonus points on? The more important question is, CAN you spend those bonus points on what you want? Each card company has its own rewards program and set of points. The rules vary widely on whether they can be cashed out, transferred, or with whom they can be redeemed against. Bonus point awards often take 6-8 weeks to post to your account after meeting the minimum spending, so if you are pressed for time, you may not be able to capitalize on those sweet bonuses. The moral of the story is, have a clear goal on what you want points for.

Who Should Absolutely NOT Churn

If you have ever carried a credit card balance, if you have ever been late on a payment, if your credit score is below 720, if you have ever had a library fine for returning a book late, credit card churning is NOT for you. You need to be meticulous!

Getting Our Toes Wet

We have plans to travel to Costa Rica later this year, so our goal is to reduce the cost of that trip with credit card churning.

This morning after doing plenty of research, I applied and was approved for the Capital One Venture card. I chose this card for several clear reasons.

The Venture card was one of the only cards that let you apply points retroactively (within 90 days) against transactions in your statement history. This is very important due to the timing of the trip we plan to take. If you add up the 3 months of spending to reach the min spend, and then an additional 2 months to have the bonus points post, you are already at five months from now to when you have points that you can use. Assuming that you book your airfare at the recommended 6 weeks pre-travel, you are looking at almost 7 months lead time from applying to a card to when your trip is going to be.

Another reason to go with Venture is the flexibility of using points. Any transaction that posts as travel can be redeemed against. You are not locked into a particular airline or hotel chain.

The minimum spend was within our capabilities. There are some fantastic business card sign up bonuses out there and some bigger personal bonuses, but they all have higher min spends. As a frugal family, we just don’t spend that much to meet those higher limits.

The 2x miles for every dollar spent means that the actual cash value will be ($3000 min spend * 2) + 40,000 bonus = 46,000 points = $460 in travel reimbursement. If Shae also signs up for a card that will be $920 of ‘free’ travel.

I applied online and was approved right away. Satisfyingly, my free account with Credit Karma sent me an email almost instantaneously informing me about the hard inquiry.

As expected, my credit score took a hit.

Keeping calendar reminders and detailed records is a must.

I will have to do a follow up post when/if we succeed in our first credit card churn. I am a bit concerned about meeting the min spend on two cards, but if we do some of the home improvement projects we have been considering, it shouldn’t be a problem.

Leave a comment if you have churned before or if you have a question about churning.

I read an interesting blog post about a month ago that talked about the effect of early retirement on social security. The writer concluded that retiring early on a high income was essentially the same as working longer at a lower income. In essence, the total amount of income is more important than time in the system.

The reasoning behind this is how social security payments are calculated. The SSA, Social Security Administration, uses a formula to calculate ones benefit. That formula works off the PIA or primary insurance amount. The PIA formula uses a sliding scale and the average indexed monthly earnings (AIME).

Confused? Good. Then we were in the same boat the first time I read through this as well.

An example and charts will help explain the whole mess.

AIME

For starters we have the AIME, average indexed monthly earnings. Simply put, this number is how much you have earned in a 35 year period divided by 420 (35 years * 12 months). If you made a million dollars ($1,000,000) over the course of 35 years your AIME would be $2381 (they get rounded to the nearest whole dollar).

If you work more than 35 years, the lowest working year incomes are tossed out. If you work less than 35 years (early retirement) then the empty years are filled with zeros and that drags your AIME down.

Finally, in order to qualify for SS, you have to earn 40 work credits. You can earn up to 4 credits per year. To simplify, you have to earn money for at least 10 years to qualify for your own SS benefits (non-spousal).

You can look up your current work credits and earnings income on ssa.gov.

Now that we have an idea of what AIME is and what your AIME number could be, let’s see how the PIA formula plays out.

PIA

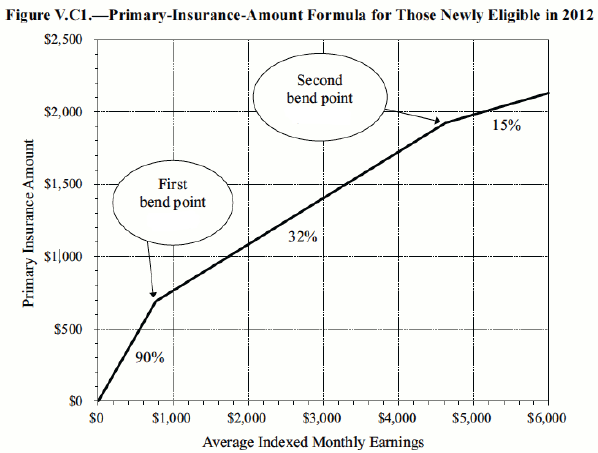

PIA works on a sliding scale. The first $856 of your AIME pays out at 90%. The amount of AIME between $856 and $5157 pays out at 32%. Anything above $5157 is paid out at a measly 15%. Graphically, it would look something like this:

Let’s consider two hypothetical men Mr. Management and Mr. Pleb. Management has done quite well for himself and his AIME is $6000 ($2.5 million earned over 35 years). Pleb has an AIME of $3000, half that of his middle management boss.

Using the PIA formula we can figure out the social security benefit for each man.

Mr. Management would get:

($856 * 0.9) = $770. This is before the first bend point

Plus

($4301 * 0.32) = $1373. This is between the two bend points

Plus

($843 * 0.15) = $126. This is after the final bend point

His total benefit would be $770 + $1373 + $126 = $2269/mo

You can see how the sliding scale makes the first $850 yield so much more than the last $840 dollars (770 vs 126). Social Security was designed to be a progressive system and is inverse of our progressive income tax system (the rich pay more and get less).

How about Mr. Pleb?

($856 * 0.9) + ($2144 * 0.32) = $1456/mo.

Mr Pleb made half as much as his boss, but will get more than half in social security.

How is this Useful?

Now that we know how the system works, we can game the system. It should be obvious that reaching the first bend point is critical to maximizing ones benefit. It should also be apparent that exceeding the second bend point is rather pointless in terms of benefit returns.

To fill up the first bend point, you’ll need to earn $359,520 over the course of 35 years (~$10k/year). It doesn’t matter if you earn 10k a year for 35 years or 360k in one year and nothing in other 34 years. Your SS benefit will be the same.

Social Security lacks returns once you cross over $2,165,940 of earned income (~$62k/year).

To game the system, try to earn as closely to 2.1 million as possible. Once you’ve made that, you can stop asking yourself if working longer is worth it for a bigger SS check. If you don’t make it to that amount, don’t sweat it. The really important bucket to fill is that first 90% payout.

With the end of the year in sight, it is time to do our annual tax forecast. Shae and I like to gather up our numbers and estimate how much of a tax liability we will have in April. Now is a good time to do it because there is still time to make adjustments to IRA contributions and 4Q estimated payments (due in January) for my business.

A really simple tool to use is Intuit’s TaxCaster. Intuit is the company that makes TurboTax and Mint.com. After putting in our numbers, it looks like we’ll end up overpaying if we stay the course.

Our total tax bill will be about the same as 2014 even though we made more money in 2015. We were able to squirrel away more income into tax deferred accounts such as 401ks and IRAs this year. Self employment tax continues to be a major bane as there are no loop holes to get out of it. Ugh!

For 2016 our goal is to drastically reduce our tax liability by fully funding our retirement accounts. This year we finished paying off our house so we shouldn’t need as much cash flow in the coming year. If you want to read a truly inspirational account of one couple paying a meager $150 in income taxes on $150,000 income go read this blog post here. Spoiler alert, the answer is to shove as much money into tax sheltered accounts as possible and have lots of kids (ok, just 3).