I wrote exactly one month ago about how we had paid off our mortgage (see here). Simply sending in the last payment to a mortgage is not enough however. To truly be finished with a loan, whether that be a student loan or a mortgage, you need the paperwork to back it up. For mortgages, that comes in the flavor of a Release from Mortgage. Basically the lender says, “Yup, they done paid in full” except in writing and usually in a more educated manner.

That piece of paper does more than just give you a warm fuzzy feely. When it comes time to sell your house, the buyer is going to want proof that no one else has a legitimate claim to the property. A mortgage after all is just a secured loan, with the security being the property. So I took that nicely worded piece of notarized legalese and went down to our county clerk/recorder’s office to have it filed for $33. The clerk/recorder’s office keeps a record of all property deeds, mortgages, liens, and foreclosures. These public records are commonly available online for easy searching. It makes it very easy to research properties and also to be very nosy. 😉

Anyway, we now officially own the deed to our house free and clear. No other parties have any legitimate claim on it and the process of selling will be slightly simpler.

screenshot from county recorder’s website

Shae’s name is on the deed. I don’t know why it isn’t listed on the Grantees list, but it is where it counts.

Ahh, the afterglow of the shopping event of the year. This year we splurged on a new mattress for our guest bedroom. It was past time to replace the mattress of unknown age that I picked up at a second hand shop. Spending money on items between you and ground is something that I am less frugal about. Shoes, mattresses, and tires are just some of the things that I will gladly shell out a little extra on.

This year, Lowes’ Black Friday deal ended up sucking me in. They had a deal on LED lightbulbs for a buck a piece. I couldn’t believe how cheap that was, and yet I was a bit wary. Two years ago we shopped for TVs during Black Friday and from that experience I knew that manufacturers make special product models just for BF. These special productions runs usually cut corners and produce an inferior product. Two years ago, we ended up getting a name brand regular tv model on clearance for the same price as a BF generic. A decision I do not regret.

So color me unsurprised when I went into Lowes (on Monday, I’m not crazy enough to go on Friday) and saw that the expected life of these super cheap LEDs was only 2000 hours. Most LEDs have expected life 5-10 times as much for 2-3 times the price. Still, I loaded up a cart and swapped out most of the CFLs in our house.

Now for the math, was it the right decision?

Most of the CFLs replaced were 13 watts and had been installed about 3 years ago (~1/3 of expected life).

The LEDs are 9 watts and our electric rate $0.0912087/kWh (taken from our last utility bill).

I wanted to find out how many hours of life I needed to get from the LEDs to break even at $1. The difference between the CFLs and LEDs was .004 kWh.

2741 Hours

Damn, I screwed myself.

The good news is that if you are replacing a higher wattage bulb, say a 60 watt incandescent, the math works out favorably. In that case you only need to get 215 hours of life out of these cheapo LEDs to break even.

I guess I can console myself with the fact that the replaced CFLs were already 1/3 into their stated lives and CFLs contain mercury. Also, I did pass those CFLs onto neighbors who replaced incandescents. Yay for the world, boo for not doing the math beforehand.

Today a great mystery was solved when we were finally able to answer the long burning question, “What goes bump in the night?”

It all started back on May 21st, 2014. Shae and I were laying in bed and dozing off to sleep when we heard it.

chtchtcht chtchtcht chtchtcht

“what is that noise?” I thought to myself while laying in bed.

“Did a bat get in, it sounds like it is coming from the ceiling”

I flipped the light on. There was nothing flying around the ceiling.

chtchtcht chtchtcht chtchtcht

The sound moved across the room over to the wall.

“Maybe a squirrel or raccoon got into the attic?” I said to a groggy Shae.

Tepidly I opened the attic door and walked up the steep steps. Hmmm, maybe I should have brought along some sort of weapon to fight off a rabid coon. gulp!

I made it to the top of the steps and gingerly set the light dimmer all the way down so as not to enrage the beast. <flip>

Nothing. I peak around the area above our bedroom and fail to see any intruder. I crank the lights to full brightness just to make sure the neighbors know how strange we are.

I walk back downstairs and see Shae staring at the bedroom ceiling right above where we sleep every night.

chtchtcht chtchtcht chtchtcht

A year later…

and the mystery noise made another appearance. As we tossed and turned in bed trying to not think about the critter walking around feet away from our heads I devised a plan.

The next morning I cut a hole in the attic floor.

Our bedroom has a drop ceiling that is hung from 1×2 strips. Above that is the original lathe that held the now gone plaster. Then above the lathe are the joist bays. The drop down ceiling provided the perfect place for critters to scurry around unobstructed. My plan was simple. Break a section of lathe so that any critters could more easily move between the drop down section and the joist bay, then place traps within the joist bay. Finally, I replaced the cut out section of flooring.

After a few days of checking the traps and not seeing any results I left them alone and then forgot about them. It wasn’t until today when we were cleaning up the attic that I checked them for the first time in months.

Sure enough, the home invader had been stopped with deadly force.

It must have triggered the trap shortly after I had set it because the corpse was thoroughly desiccated. Now we know what goes bump in the night.

Parents tripping over toys and little mice scurrying around the joists.

A note about frugality and humane killing

Old fashioned mouse traps like these are cheap at less than 50¢ a trap. They are also a very humane way to get rid of mice. They are designed to break the neck of the mouse, which would be a near instant death. The last thought of this mouse was most likely, “wow this peanut butter tastes great”.

929 days, or 2 years 6 months and 16 days, or simplified even further 2½ years from the day that we took on a mortgage to the day that we killed it.

2½ years ago we bought our house with a 15 year mortgage. By living a frugal lifestyle we were able to make quadruple payments on our mortgage and be debt free in only 2½ years!

Mortgage Balance

Being debt free is a huge step towards financial independence, the ability to dictate where, when, what, and with whom you work. For many people, financial independence is commonly realized as retirement. A time when you can pursue your own interests and not have to depend on a paycheck.

For us, our monthly mortgage payment was the single largest monthly budget item. Now it is a thing of the past and let me tell you, it feels liberating!

I often think of mortgages in two ways. The first way is that a mortgage, just like any other type of debt is a pay cut that you negotiate for your future self. If you make $50,000/year and you take on a $500/mo payment, you have effectively given yourself a pay cut of $6,000. Earning less is no fun, but that is essentially what debt does.

The other way that I think of mortgages is to visualize the rooms of your house. We have about 12 distinct areas of our house (foyer, living room, dining room, kitchen, basement 1, basement 2, bedroom 1,2,&3, master bath, attic). Our mortgage was 33% of the value of the house, so the bank ‘owned’ four of the twelve rooms of our house. For people that only put down 1-2% on a house and take a loan for the other 98-99% they only have a few square feet to ‘live’ in because the rest belongs to the bank!

Of course, any discussion about paying off a mortgage has to include the age old argument, “is mortgage debt good debt?” This is an argument that is entirely personal in nature. Camp good debt argues that with the historically low interest rates that homeowners can secure 3-4% it makes more financial sense to make minimum payments on mortgages and invest the rest into the stock market in the hope of earning 7-10% there. The 3-6% profit makes mortgages an easy source of leverage. The other camp argues that paying off a mortgage is a guaranteed 3-4% and it is too risky to leverage your home for stock purchases.

I would argue that any debt over inflation (about 2%) is bad debt and any debt below inflation (less than 2%) would be good debt. I say that with the major caveat of this being personal debt. Businesses is a whole different ballgame.

So what was our grand super duper secret for paying off our mortgage so quickly? In three words,

below our means

The house that we bought was a foreclosure put up on auction. We could have bought a house twice as expensive with the mortgages offered by big banks. Instead we bought a fixer upper.

The Day We Moved In

This house had sat empty for three years. While that made the price drop down into bargain territory, it also made for some hefty elbow grease.

New Water Heater Required on Day 1

toilet didn’t even have a seat

leaky plumbing everywhere!

pony up more cash for missing appliances

Sweat equity moving and installing ourselves

Thankfully, we had family that pitched in to help us move and install a number of appliances.

moving new refrigerator

installing a new dishwasher

sliding a dryer down the stairs

Sister-In-Law cleaning up the bushes

Planting flowers

Thank you!

It has been quite the journey. Being frugal and saving money is a means to an end. For us that includes being debt free!

Now What?

Now we will redirect that mortgage payment money so we can max out our tax protected retirement accounts. Once those are maxed out, any surplus money will be spent on whimsical fun things! Hurray delayed gratification. ?????

In honor of my brother buying his first house, I thought a cost of home ownership post was appropriate. Maybe this will be a spooky Halloween post for him and other new homeowners around the world or it will be a shot of encouragement.

For the past five months I have been rebuilding our front porch. The old porch had a failing foundation and was looking like it could fall down at any moment. When we bought the house we knew we would have to do something about it, and two years later we finally did. So before we get into the numbers a bit, let’s take a look at a before and after picture.

Everything from the roof down was demolished and rebuilt. While I did most of the work by myself, I did have quite a bit of guidance from our next door neighbor who is a professional carpenter. Shae helped with painting and decision making. Additionally, we hired a mason to lay new brick piers and a flooring contractor to sand the new/reused porch flooring.

With November only a week away and winter not far behind that this project is likely being shelved until next spring. There are still handrails to finish up, skirting, and a lot of touch up painting needed to officially mark the job as complete.

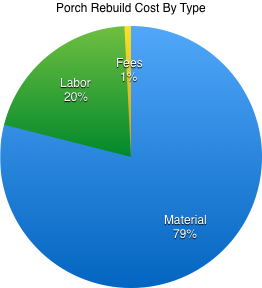

So you ask, what did it cost to get this far. $4235.03. Of that, raw materials was 79%, hired help was 20%, and bureaucratic fees made up the final 1%.

Our material cost was driven up by our choice to reuse the existing ipe flooring. Ipe is an extremely dense and rot resistance Brazilian hardwood. We were able to salvage about 70% of the existing flooring and reuse it, but the other 30% plus new stair treads in matching ipe accounted for 43% of our material cost at a total of $1438.66.

Another area we splurged on was the foundation work. We could have stuck a treated 6×6 into the ground and poured concrete around it and called it a day. Instead we dug huge holes to make large concrete pads to support brick piers (that were themselves filled with concrete) to support the framing.

The extra strong foundation was $1274.95 (793.95 in materials + 485 in mason labor). Our justification for spending so much on that was two fold. Firstly, if the foundation had been done properly the first time around, we wouldn’t have had to do this project. Secondly, a wood post in the ground would not match the historic nature of our house and neighborhood. It would also eventually rot out and that brings us back to our first reason.

Once you take out those two big ticket items we are left with $1521.42. That covers all of the framing lumber, painting, tools, a professional sander, permits, and misc. nickels and dimes.

Okay, I know I know. I left out the biggest cost of all in the numbers above. My time. I have been working on this on and off for the past five months and that has value. I do not know how many hours I put in, but I do know what local costs are for hiring out a job like this to a contractor. Let me just say, my time investment has been worth it. We have easily saved five figures by doing the work ourselves. All you have to do is take a look at the Labor portion of our costs and see that just two guys ate up 20% of the project cost. Imagine what a full team working for a couple of weeks would do!

Good luck with your new house bro. They are expensive and time consuming but for us, that beats the alternative of sharing a wall and roof with someone else. So roll up your sleeves and start building some sweat, blood, and tears equity!