This morning, Shae and I opened a kid’s savings account for Frugal Boy. We were able to do the entire process online in about 10 minutes including the initial funding requirement of $25. Later on, when the bank was open, Grandpa and I took Frugal Boy to a brick and mortar branch to deposit his very full doggy and piggy bank.

He looked ready to ride his money all the way to the bank.

The grand total of his little banks was $41.10. Thankfully, he was not sad about emptying out his little banks. In fact, he was kind of the opposite. When we got back to the house, he went up to Grandma and asked her for more money to fill up his now empty banks. Umm, we still have a lot of parenting work ahead of us.

In the future, any cash gifts Frugal Boy receives will go into his savings account. Any checks will continue to go into his 529 College Fund unless otherwise requested. In another year or two when he better understands the concept of money, we will probably switch all of his gifts towards his savings account.

Thank you to everyone that has gifted Frugal Boy with money over the years. We are trying to teach him how to be frugal and know the value of a dollar.

We are another day closer to having a tiny helpless human being in our house again. Umm, is there a timeout button somewhere that I can push? Shae has been nesting, er collecting some of the infant paraphernalia that we shed when Frugal Boy outgrew it. One of those items is a new, used neglect-o-matic. For all of you normal folks out there, I believe the politically correct term is ‘Excersaucer’.

Frugal Boy was all to happy to help set it up and test out all of the different dingle dangles.

I’m wondering when he will grow tired of it. He has been playing with it the entire time that I wrote this post. Did I mention that it makes a lot of noise? At least the price was right. FREE!

Earlier this week, I came across a nifty resource at socialsecurity.tools. The website, made by an individual not the government, helps provide a clearer picture of what one’s Social Security benefits will be at different ages and different working year earnings. This is particularly helpful for planning a retirement that is before the normal age of 65 or when you expect your earnings to significantly change up or down in the coming years. As it stands, the official SSA.gov website only gives very generic estimates about your SS benefits and it only does so after you have earned the prerequisite 40 working credits, something that is difficult for anyone in their 20s to accomplish (because you can only earn a maximum of 4 per year).

Seeing as this tool was created by a stranger on the internet and deals with personal finances, it is prudent to check the security and safety of the site before entering numbers. The about page has this to say about Security.

Security

This site does not store any data entered by users. All calculations are made client-side in the browser’s JavaScript and are never transmitted over the internet.

While unnecessary for security, this can be confirmed by loading the site in your browser, and then disconnecting your computer before entering any additional data.

Yes, it is safe to use. Furthermore, it is really interests you, the author of the tool has made the source code public on GitHub.

You will need a free SSA.gov account in order to use the tool. SSA.gov keeps a record of your earnings that you will copy and paste into the tool. Once you have done that, you’ll see a screen that looks similar to this (I used one of the demos for all the screenshots below, they are not my numbers).

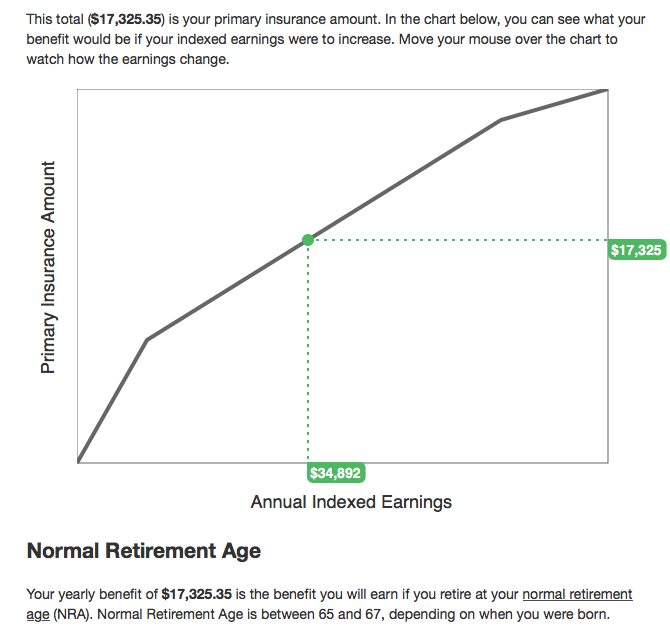

Additional information is available as you scroll down the page. You may recognize the PIA vs AIE ‘bend-point’ graph from one of my previous blog posts. With this tool, you can see where exactly you’ll be on that graph.

Finally, farther down, you can get an idea of how your benefit will change depending on when you start taking it. Currently, age 62 is the soonest that you can begin taking benefits. It also carries a -30% penalty. You must start taking benefits by age 70, and waiting that extra time caries a 24% increase in yearly benefit payout.

I would encourage you to check out this tool, doubly so if you are in your twenties or thirties. One of the greatest misconceptions about retirement planning is that it is something that you do when you are in your fifties or sixties. Retirement planning is best done early in your career so you have time for compounding interest to work!

One interesting thought experiment when planning for retirement is thinking about your coast number. What is a coast number you ask?

Let’s take an imaginary man, Frank, for our little thought experiment. Frank is diligently saving 20% of his income into a 401K or IRA that is mostly invested in equities. For arguments sake, the retirement vehicle will produce 7% returns every year. Frank wants to retire at the age of 65, when he can pull social security benefits. If Frank front loads his retirement savings, there may come a threshold when he can stop saving 20% of his income because the investments will grow enough on their own to secure his retirement at age 65.

That threshold, is what I am calling the Coast number.

To calculate the coast number, we need 3 inputs. We need to know or guesstimate the Rate of Return that the investment vehicle will kick off every year. We need to know the goal amount to be saved and we need to know how much is currently saved towards the goal.

The continuous compounding formula is A = Pert where A is the goal amount, P is the starting amount, r is the rate of return, and t is the time it takes to get there.

Say Frank wants $25,000 a year from just his retirement savings after he turns 65. According to the 4% safe withdrawal rule, he would need a total amount of $625,000 in retirement savings to do that. If he has already saved $75,000 then we can calculate his coast number.

(1/r) * ln(A/P) = t

(1/.07) * ln (625000/75000) = t

t=30.29 years.

Subtract 30.29 years from his planned retirement age of 65 and we can see that he can stop contributing to his retirement accounts and coast on the savings a little before his 35th birthday.

Of course, for the majority of the population, the coast number would be somewhere in our past. The whole point of this exercise is to see if you front loaded your retirement savings to take advantage of compounding interest, when could you theoretically stop saving for retirement.

You can use the calculator below for your own hypotheticals. They don’t have to be retirement related. Perhaps you are saving up for a house down payment or other large expenditure.

When I was growing up, we would make an annual or biennial road trip to visit my Grandma in St. Paul, Minnesota. It was a full day or sometimes even two day car ride and it was BOOORRRIINNG. I don’t mean the car ride itself was boring, of course that was, but also the destination portion as well. To add insult to injury, the route to and fro always passed by Lake Delton, home to Wisconsin Dells and some of the largest waterparks in the world. I always remember looking out the window as we crept along the interstate and wished that we would stop there instead. It would have been a lot more fun than the regularly scheduled program.

A kid can dream

Alas, we never did stop at the waterparks on our way to Grandma’s. As an adult, I understand my parents reasoning. Firstly, it is expensive, especially when you have a station wagon full of kids. Secondly the purpose of the road trip was to visit home bound family members.

30 years later and kid me got his wish fulfilled! Shae’s work puts together discount trips throughout the year. We decided to take advantage of one such trip that was a two night stay at America’s largest indoor waterpark, the Wilderness Resort in Lake Delton, WI.

3 Charter Buses Caravanned

a small part of the mega resort

3 indoor waterparks for the price of 1

The room cost was $386.27 for both nights, and the bus ticket cost was $25 per person. We also spent $85 on dinners, and another $14 on breakfasts and lunches. The total trip cost was $560.27 including all transportation, lodging, food, tickets, taxes, fees, and gratuities. Per person, that comes out to $186.76 or $93.38 per day. We could have included a 4th person for just the bus fare of $25 plus food. One could easily argue that this was not a frugal trip.

We did save gas money by riding on the charter bus, so that was probably $40 saved. We also saved quite a bit of money by bringing breakfast and lunch staples from home and only eating out for dinner. Finally, the room rate was a special group rate. We saved $15 with the Group Rate for lodging.

There are three separate indoor waterparks at this mega resort, and we tried them all out over the course of two days. All of them had a mix of little kid/teen/adult attractions. Shae couldn’t partake in any of the slides because she is sporting a wonderfully cute baby bump.

Frugal Boy at a stout 37″ was able to go with me on probably 50% of the slides. The two of us had a great time riding tubes and rafts down dark passageways. At the end of the trip, he said it was his favorite part. Ahhhh.

Some areas were included in the lodging price, such as this three story play area.

It was a lot of fun climbing around the structures and using the air cannons to shoot nerf balls at other people.

Frugal Boy loading a mega cannon.

a little teamwork

multi-story slides are fun!

We skipped other areas that were pay-to-play, such as the Arcade and High Ropes course.

my nephew would be begging to go on this.

We had packed breakfasts and lunches from home to save money on eating. I was pleasantly surprised with the cost, quality, and service of the dinner choices. I was expecting concession stand quality food at huge markups in cost all paired with crappy service. Instead for dinner we had decent food with quick friendly service at only a modest ‘tourist trap’ markup in price.

Frugal Boy contemplating what he wants for dinner

When we travel, we try to stick to our normal bed times. For Frugal Boy that is 7pm, so like it or not, we tend to have a lot of downtime during the evening. One of the tech items that I really enjoy is Plex. Plex lets you serve up your media collection at home to anywhere in the world. Now when we travel, we can bring along an old laptop, or our Apple TV and we can watch all of the same movies and tv shows that we can watch at our home theater. When Mom and Dad just need a moment, Paw Patrol is still one of the best distractions.

It will be nice when the kids get a bit older and do activities later into the day. For now though, we’ll just enjoy the cuddles.

The company does the same, or very similar, bus trips each year. Next year, we’d probably skip this trip because there is not a lot that a one year old can do at the park.

While it was an expensive weekend getaway, it was a lot of fun and our last 3-person trip before our family dynamic changes. Shae and I both wanted to enjoy and savor the last bit of time that we have with Frugal Boy as an only child.