Earlier this week, I came across a nifty resource at socialsecurity.tools. The website, made by an individual not the government, helps provide a clearer picture of what one’s Social Security benefits will be at different ages and different working year earnings. This is particularly helpful for planning a retirement that is before the normal age of 65 or when you expect your earnings to significantly change up or down in the coming years. As it stands, the official SSA.gov website only gives very generic estimates about your SS benefits and it only does so after you have earned the prerequisite 40 working credits, something that is difficult for anyone in their 20s to accomplish (because you can only earn a maximum of 4 per year).

Seeing as this tool was created by a stranger on the internet and deals with personal finances, it is prudent to check the security and safety of the site before entering numbers. The about page has this to say about Security.

Security

This site does not store any data entered by users. All calculations are made client-side in the browser’s JavaScript and are never transmitted over the internet.

While unnecessary for security, this can be confirmed by loading the site in your browser, and then disconnecting your computer before entering any additional data.

Yes, it is safe to use. Furthermore, it is really interests you, the author of the tool has made the source code public on GitHub.

You will need a free SSA.gov account in order to use the tool. SSA.gov keeps a record of your earnings that you will copy and paste into the tool. Once you have done that, you’ll see a screen that looks similar to this (I used one of the demos for all the screenshots below, they are not my numbers).

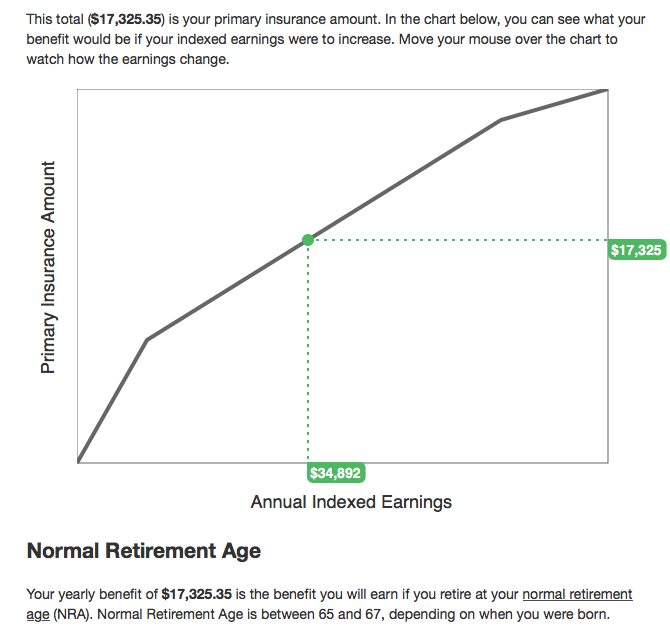

Additional information is available as you scroll down the page. You may recognize the PIA vs AIE ‘bend-point’ graph from one of my previous blog posts. With this tool, you can see where exactly you’ll be on that graph.

Finally, farther down, you can get an idea of how your benefit will change depending on when you start taking it. Currently, age 62 is the soonest that you can begin taking benefits. It also carries a -30% penalty. You must start taking benefits by age 70, and waiting that extra time caries a 24% increase in yearly benefit payout.

I would encourage you to check out this tool, doubly so if you are in your twenties or thirties. One of the greatest misconceptions about retirement planning is that it is something that you do when you are in your fifties or sixties. Retirement planning is best done early in your career so you have time for compounding interest to work!