Instilling a Saver’s Mentality on Kids: Then and Now

Shae and I hosted Thanksgiving this year and my parents handed me an envelope filled with banking receipts covering years of my childhood. It could have just as easily been shredded, but since I have it, I might as well delve in and examine some of the financial going ons of my childhood. I have vague recollections of particular financial events, such as diligently depositing birthday and Christmas gift money, but now I have the receipts to piece it all together.

Then

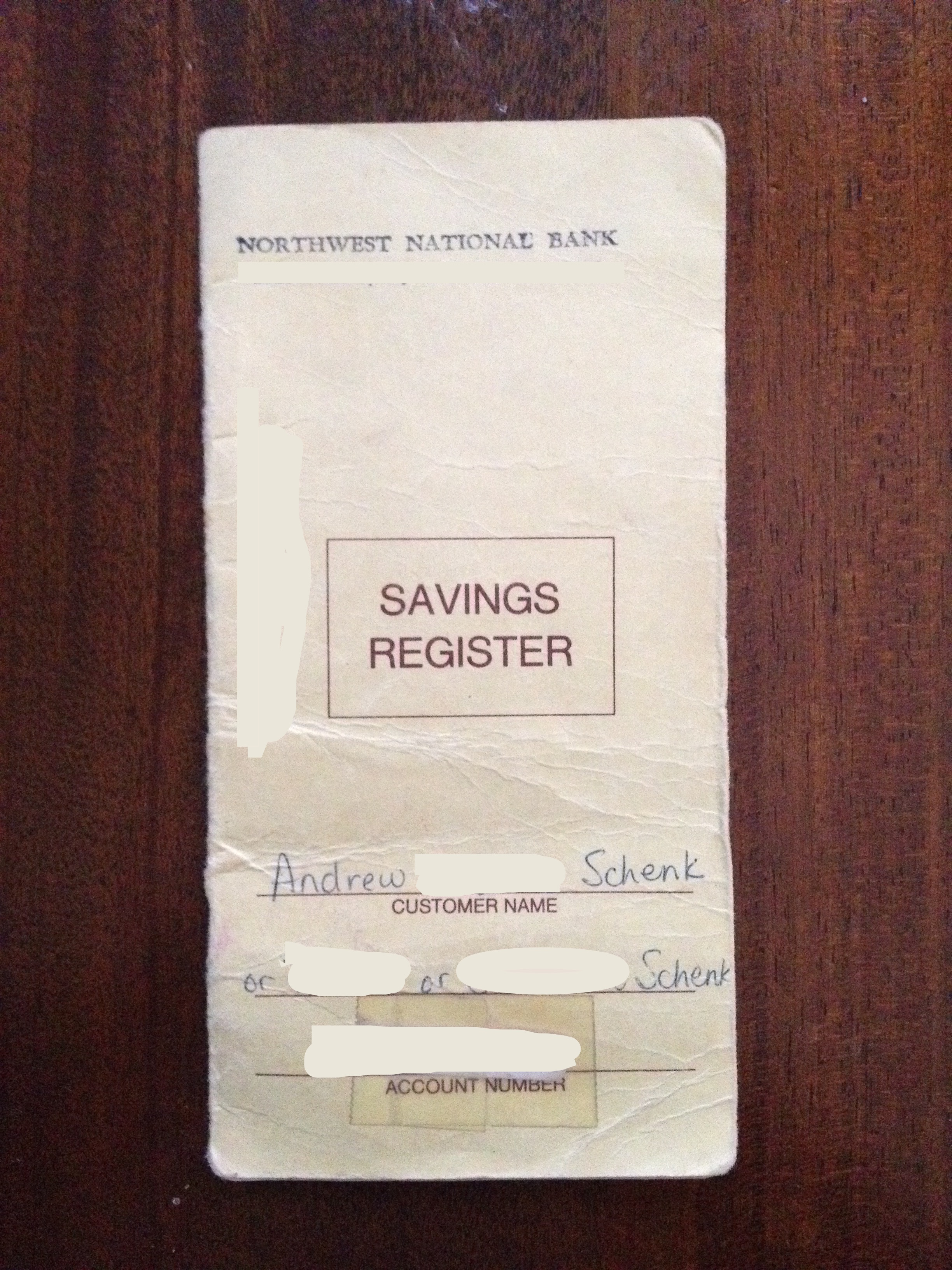

It all started when I was 3 months old. My parents opened up my first bank account. Gee, thanks Mom and Dad. Back in the olden days, there was no online banking. So I had a Savings Register to record transactions in.

Opening up the register, you can see the first deposit, and subsequently, how old I am.

That $310.00 adjusted for inflation would be equivalent to $660 in 2016. Thanks Grandparents, uncles, aunts, and family friends for pitching in for my financial future.

Over the years, the balance steadily grew. I particularly like the 4th or 5th grade me that deposited $25 of ‘prize money’ in 1998.

I have no memory of what contest I won back then, but an interesting thing begins to happen around that time period. The handwriting changes, and some of the entries are being made by a little boy.

Around junior high school, middle school, or whatever you call 6th, 7th, and 8th grades, I had saved up enough money, at my parents behest, to start meeting the minimum requirements of Certificates of Deposits, or CDs for short. I do remember my Dad always shopping around the 4 or 5 banks in town looking for the best CD rates. I also remember him on a trip up to Grandma Schenk’s house once bemoaning the fact that she did not shop around rates and was leaving money on the table by being loyal to the same bank forever.

Anyway, in ’00, there is a receipt of a CD being closed.

At age 13, the saver mentality had been thoroughly beaten into my head by my parents and I had approximately $3,000 to my name, the bulk of which was tied up in a CD.

Birthday’s and Christmas’s kept rolling by year after year, and year after year I would write a fistful of thank you notes to grandparents, uncles, and aunts before dutifully marching down to the local bank and depositing checks and cash. At some point my Dad made me go alone and stopped helping me fill out the deposit slips. Of course I was terrified, but it was a good sink or swim lesson.

My Dad kept optimizing the best savings rates for me and kept the bulk of my savings locked up in CDs.

This particular CD was kept open for 2 years before being closed. The grand total of interest earned over that two years was $231.47.

In 2004, I began working and earning money for myself. The pay was negligible, but the real payoff was learning the value of a dollar. Performing a mind numbingly boring task for hours on end to collect a small paycheck gives one plenty of time to think. Suddenly, that new flashy item being marketed to you seems a little less interesting when you replace the dollar cost with an hour cost. Something that costs $50, is the same as something that costs almost 10 hours of work for someone on Indiana’s minimum wage of $5.15/hr. Yes, that was what I started at. Spending several hundred of my own dollars to take a girl to high school prom did not seem like a balanced equation. A couple of hours of fun was not worth the 50 hours of work required.

Finally in ’06 as a senior in high school, I opened up my first solo bank account. I was now 100% in charge or my own finances. The rest as they say is history.

Now

Now the tables have turned. I am in the role of Dad, and Frugal Boy and Frugal Fetus are in the role of child. Just like my parents handled all the finances when I was born and slowly relegated duties to me over the years, Shae and I are doing the same with our children. Frugal Fetus doesn’t know it, but he/she already has a college savings plan opened up and partially funded. In fact, since it was opened in July, it has returned 6.83% APY. Frugal Boy’s 529 college savings plan has returned 8.95% APY for the year-to-date. On a more concrete level, any cash that Frugal Boy receives he diligently stores in his doggy bank at his parents behest. Any checks are invested into his college savings. Amusingly enough, Frugal Boy already recognizes and calls out the different bank branches as we travel through town. I think he is almost ready to graduate to his first real bank account. We will probably open a PNC ‘S’ is for Savings account for him. It has 0 fees for age 18 and under account holders and uses Sesame Street characters to encourage kids to save.

There are a number of savings programs available for kids. Here is a roundup of some of the more popular ones.