Yesterday for Mother’s Day, we loaded up in the car and drove to Blackhawk Springs Forest Preserve for a picnic lunch.

It was a nice sunny day and several other families had the same idea.

Frugal Boy enjoyed sharing Grandpa’s cupcake.

Grandpa was a good sport.

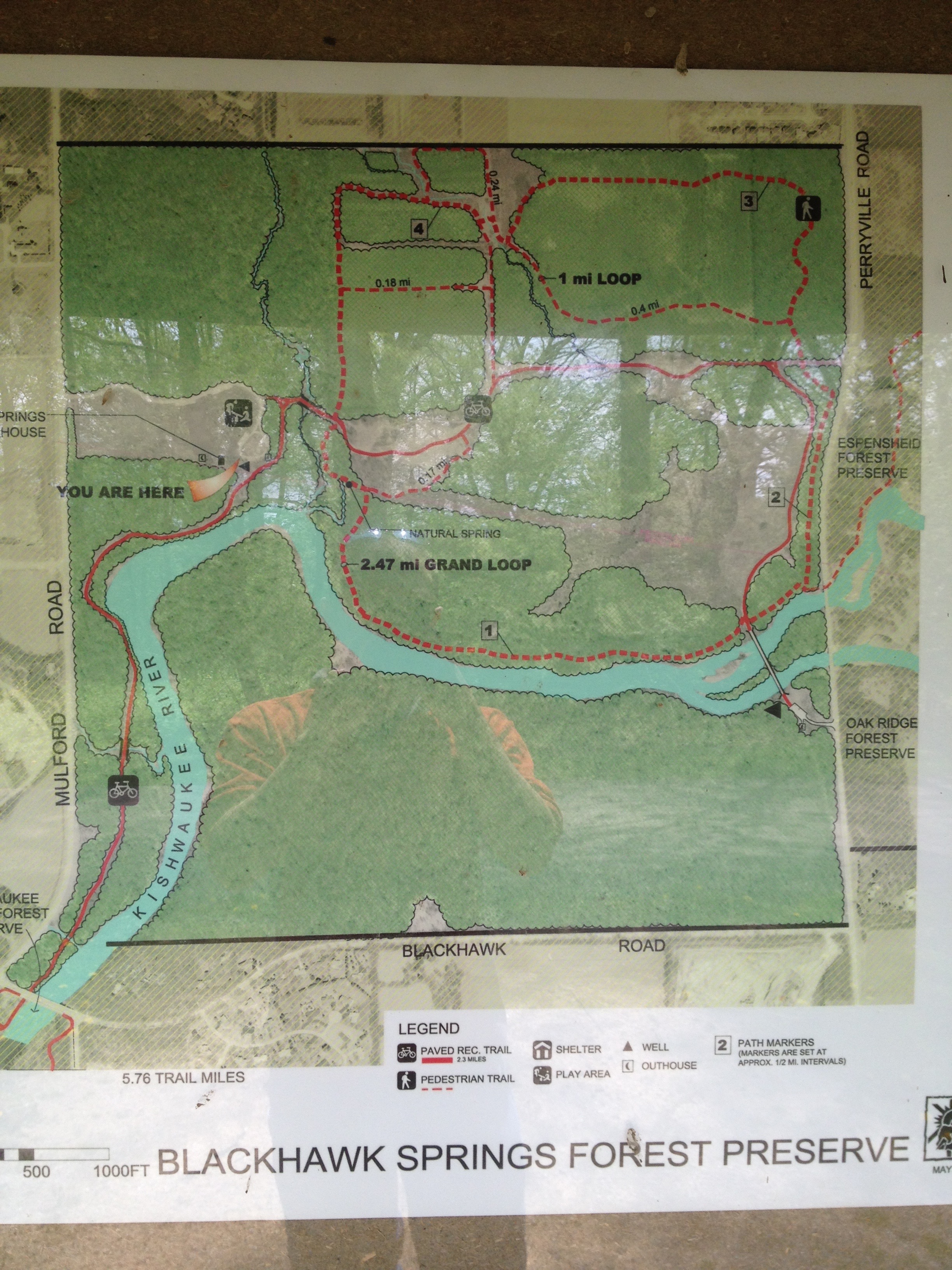

After eating a big lunch, we went for a hike. There are paved and grassy paths totaling over five miles in the preserve.

In a couple of months there will be a ton of blackberries along the trail. I saw a bunch of thorny canes just starting to set their fruit. For now though, we settled on picking some bouquets for mom.

Have you ever wondered how dandelions manage to carpet an entire area. Shae captured the process in slo-mo.

After we were finished spreading an invasive species, we found the jewel of the trail, a natural spring bubbling up from the ground. Frugal Boy got very excited and started pulling on my arm to go ‘swimming’. I indulged him and in the process gave his grandparents and aunties a show they probably weren’t expecting.

The water was very cold, but he still went back a second time before declaring all done.

Dried off and dressed, we finished up our little hike.

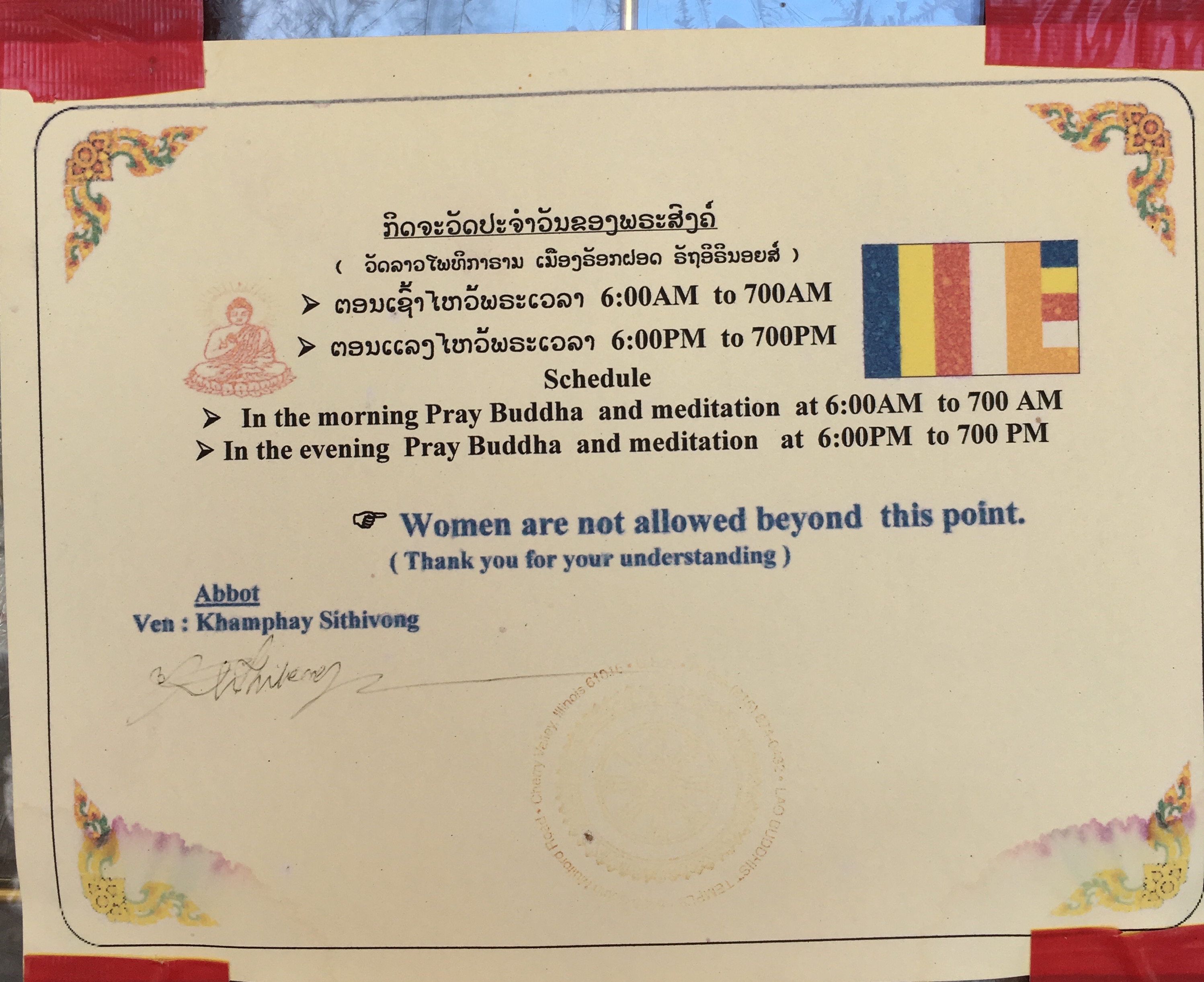

After some more time on the playground, we loaded back up in the car and drove a bit south to a seemingly out-of-place Buddhist temple. It was surrounded by corn fields and looked to be built on an old farm homestead.

A man came over and started to talk to us about the temple. Construction started in 2004 and lasted about 3 years. Everything has been done by volunteers. I was a bit surprised to see the sign on the door.

I had visited several temples in Taiwan on a college sponsored trip and they did not have that kind of restriction. From talking with the man, it seemed that this was more of a Thailand/Laos sect.

Frugal Boy liked the decorative dragons.

Leaving the temple behind, we drove to the other side of the forest preserve to look at the big pedestrian bridge.

I was impressed with the living room sized inflatable ‘raft’ that came cruising by.

I’ve been spending my free time planning out our late Spring trip to Costa Rica. The trip represents a lot of things to us, including:

Celebrating our 5th anniversary

Taking Auntie for one last hurrah before med school residency starts

Continuing our geographic arbitrage search

Celebrating my birthday and living up the last of the *careless* 20s

Enjoying our travel mobility

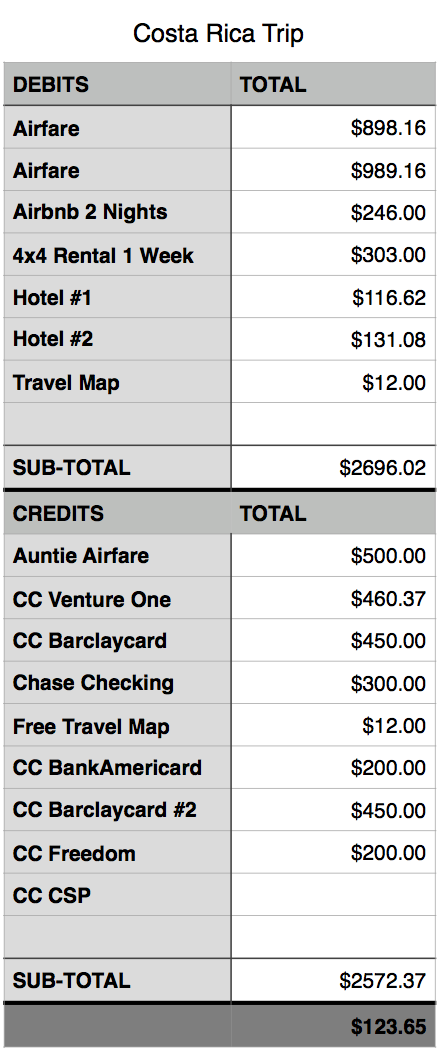

Having a good map is really helpful for planning purposes. The best reviewed map on Amazon is the Costa Rica Guide waterproof map. It doesn’t hurt that you can get the map for free by doing some advertising for them (see above link). I’ll admit, it’s why I am doing this blog post.

Saving $12 on a map might seem insignificant but it does add up. Last night while we were on our family walk, Shae and I did a mental addition of the current trip costs and credits (from card churning). With airfare for 4 people, a seven day rental 4×4 suv, and 4 of the 8 nights booked we have an out of pocket expense of around $100 so far. I figure the last four nights of lodging, food, souvenirs, and misc. expenses will push our total out of pocket expense to somewhere in the ballpark of $750-$1000 for Shae, Frugal Boy, and myself combined. I’m tempted to do one more credit card churn to knock off another $460 dollars from the total, but I don’t think we’ll be able to meet the min spend requirements. A better option might be to churn a couple of bank accounts instead (see here for a list).

It has been a little under 2 months from our first churning credit card application (read more about that here). In case you have no idea what I am talking about, credit card churning is the process of signing up for credit cards with the sole goal of collecting hefty signup bonuses from the bank. We have a trip planned for Costa Rica this summer and we wanted to see just how much money we could knock off the total bill.

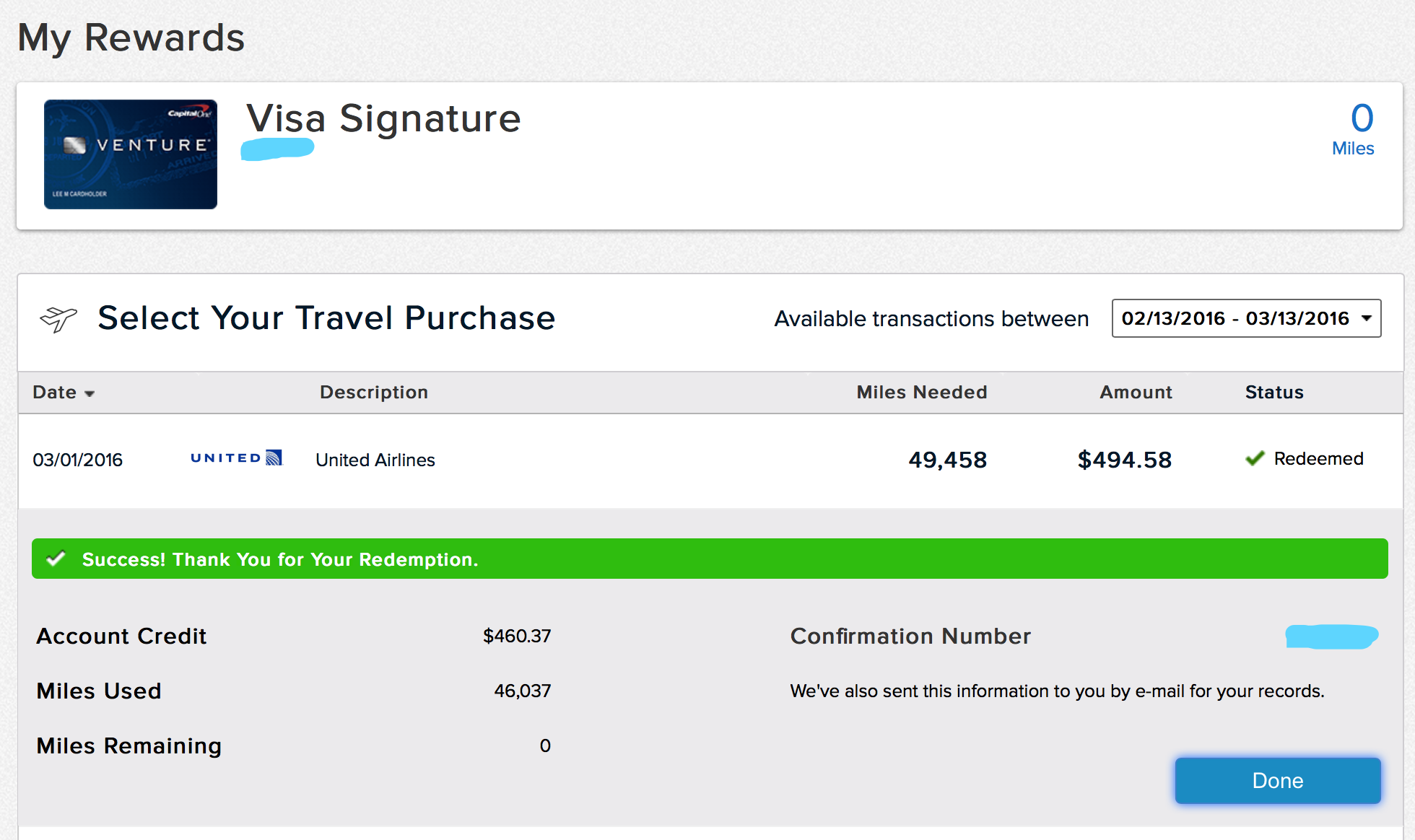

The first credit card that I targeted was the Capital One Venture card. I just completed the requirements to get the bonus for that card and the 40,000 bonus points posted soon after.

I was able to redeem the full point total against a plane ticket to Costa Rica to knock $460.37 off a $494.58 ticket. 93% off airfare isn’t too shabby!

Shae also got into the game and completed the requirements for the Barclaycard Arrival Plus. When we purchased airfare, we did it in two separate transactions so that we would be able to redeem multiple credit card bonuses against the cost.

Barclaycard Arrival + is a very similar setup to the Capital One Venture card. 40,000 bonus points are awarded for spending $3k in 3 months. One of the small differences between the two is that the BA+ card can only be redeemed in increments of 2500 points. Shae was able to get $450 applied towards a $494.58 airfare.

I am quite pleased that with two cards we were able to save $910.37 in travel expenses. That will go a long way to reducing the cost of our Costa Rica trip this summer.

But Wait, There’s More!

I’ll admit it. I got hooked. Credit card churning has been an enjoyable distraction for me. If you read the fine print, have clear goals, and a modicum of self discipline you can rack up quite a bit of ‘free’ money.

My spreadsheet has grown considerably from that initial blog post two months ago. Yes, it is color coded now according to the card issuer. Click on the image below to see a bigger more readable version.

In total we have applied for 8 cards.

Chase Freedom

Annual Fee: $0

Bonus: $150 + $50 for referer

Min Spend: $500

Min Spend Deadline: 3 months

I already have this card and it is one that I use on a monthly basis. Chase keeps sending me emails to pimp this card out to my friends and family. If someone signs up for the card through my referral link, I get $50. No, I won’t put the link on this blog.

Shae signed up through the link however so this card should net us an easy $200 and because it has no annual fee, she can hold onto it forever.

BankAmericard Travel Rewards

Annual Fee: $0

Bonus: $200 statement credit

Min Spend: $1000

Min Spend Deadline: 3 months

Both Shae and I applied for this card. Shae was approved and I was denied. Ironically, because I didn’t have enough credit card accounts. Hehehe. The plan is to use the card and bonus for Costa Rica lodging.

Chase Sapphire Preferred

Annual Fee: $89, waived first year

Bonus: 55000 Ultimate Reward Points (between $550 and $687)

Min Spend: $4000

Min Spend Deadline: 3 months

I got this card for future travel. We plan to meet the min spend by paying our property taxes with it. Yes, our property taxes are almost $4000/year. We might as well get a bonus while we rip off the tape.

IHG Rewards Club

Annual Fee: $49, waived first year

Bonus: 60,000 points + $50 statement credit OR 80,000 points

Min Spend: $1000

Min Spend Deadline: 3 months

I got this hotel credit card because it is a surprisingly good value. In addition to the one time bonus, you also get a free night every year starting on your second year of membership. Essentially, you get a $49 night at any IHG hotel. The lower tier hotels start free nights at 5-10k points. 80k reward points would be enough for around 8 free nights. If you figure those are $80 nights normally, then the bonus is worth around $640.

Chase Total Checking

Monthly Fee: $12 unless criteria are met

Bonus: $300

Bonus Requirement: Make a direct deposit of at least $500.

Bonus Req Deadline: 2 months

This one isn’t a credit card! It is a checking account. The $300 bonus was a targeted offer that Chase sent me. They really want me to be a customer, so they offered a big bonus to lure me in. The requirements are pretty easy to meet. Open it up in branch with the targeted coupon code, dump $1500 in to satisfy the monthly fee requirements, and then make a direct deposit of $500. Wait 6 months to satisfy the fine print and then close the account. Abbra Cadabra, $300 for about 3 hours of work.

Wrapping Up

All told we are looking at about $3200 in bonus churning provided that we meet the various requirements and are able to optimize the bonus redemptions. I like that I can do most of this from my computer and it doesn’t hurt that we can stick it to big companies in the process.

Speaking of Which

Did you see the credit limits that we were approved for?! Holy crap. No wonder why Americans are in debt up to their eyeballs. It is so easy to get ridiculously high credit lines. Why in the world do credit card companies think that handing out $127,900 of available credit to a couple of twenty year olds is a good idea. The morbid reason is simple, the companies are hoping we self destruct and spend more than we can pay off. If we fell into that trap, then the companies make money in insanely high APRs ranging from 14% all the way up to 22%. These companies want people to pay the minimum. So sure, give Andrew a credit limit of $25,000 and hope he screws up and becomes a wage slave. That is why I have zero empathy and zero remorse from milking these card issuers for big bonuses. I’ll play the game, but I’ll play it on my terms.

The book by Tim Leffel looks at how to get more out of your (international) vacations while spending less. Who wouldn’t want that?

I have read through the first two of three sections in the book. In section one, Tim talks about the big expenses associated with travel and how two hypothetical families, the Smiths and the Johnsons, waste and save money on airfare and lodging. The second section talks about dining, ground transportation, and souvenir shopping.

The essence of Tim’s travel philosophy is that the best trips and cheapest trips happen when we avoid the American pretense of travel. If I asked you to name a good beach destination, you would probably respond with Florida, Hawaii, or the Bahamas. The reason why those places come to mind is that they are heavily marketed. Those big budget ad campaigns come out of the pockets of tourists. In one example given in the book, a resort in the Bahamas got caught red handed publishing pamphlets of their resort with images of beaches found in Florida. Their response, “beaches all look the same anyway”. So if beaches all look the same, why spend big bucks to go to a well marketed one?

The theme of getting off the beaten track, avoiding the herd, and walking/talking/eating like a local is repeated frequently in the book. In many ways it reminded me of our recent trip to Mexico where we stayed in local apartments, ate at a food truck and other hole-in-the-walls, and swam in the local swimming hole.

I would recommend that you pick this book up and give it a read if you have ever only stayed at resorts or chain hotels, use tour buses, and never stray far from the touristy areas. If that doesn’t describe you, then you could probably skip this book.

I have heard about credit card churning for several years now and it has never really interested me before. That began to change after our Mexico trip when the lights upstairs started to flicker on about ways to trim the fat on our next international trip.

What is Credit Card Churning?

Credit card churning is the act of signing up for credit cards for the sole purpose of collecting the, usually, large sign up bonus offer. As soon as one bonus is collected you move on to the next card. Some industrious, or foolhardy, individuals may open multiple cards at once to speed up the process.

Example Sign up Bonus

Here is another example sign up bonus. This one from Capital One’s Venture card.

Why Bother?

If you do it right, and that is a very understated statement, you have a lot to gain and very little to lose. Take the Venture card for example. If both you and your spouse complete the necessary bonus steps, you stand to save $920 on travel. In the case of our Mexico trip, that would have nearly halved the trip cost!

What’s the Catch(es)?

Tons. We are talking about credit card companies who make money by taking advantage of uninformed or ill informed individuals. Here are just a few of the gotchas you have to consider.

Minimum Spending Requirement

In order to receive that big points bonus, you usually have to spend a certain amount with the card within a certain period of time from being approved. For Venture, that is $3k within 3 months of approval. If you only spend 2999, you are SOL. No bonus points for you. You might think, that will be a piece of cake. I’ll just go to the ATM and withdrawal three grand. WRONG! That counts as a cash advance and will generate 25% interest immediately. A big no-no. Serious churners who take out multiple cards at once often rely on manufactured spending, or MS for short. MS is the process of using the credit card to obtain some sort of cash equivalent and then figuring out a way to get that equivalent back into their bank account. There are many different strategies for doing this, and most of them are perfectly legal. The strategies are always changing however as loopholes are closed. I would strongly advise that you do plenty of research before going down this rabbit hole.

For myself, I am intending to avoid MS altogether and reach the minimum spending through normal usage. It is important to consider whether or not you can meet the minimum spending requirement.

Annual Fees

With high sign up bonuses, come high annual fees. The Venture card and several others, waive the fee for the first year. The card companies hope that you’ll like the card so much or just forget about it that they will be able to milk the AF for years to come. You’ll need to have an exit strategy to deal with the annual fee. Sometimes you can downgrade the card to a $0 AF, or you may have to cancel the card outright. All of this needs to be taken into consideration BEFORE applying.

Credit Score

Your credit score will take a hit from doing this. Churning is not recommended for anyone with low credit or anyone that may need credit for something important (like a house or student loan). I am in a nice position where my credit score doesn’t really matter because I don’t need it for anything vital.

Point Redemption

What are you going to spend those bonus points on? The more important question is, CAN you spend those bonus points on what you want? Each card company has its own rewards program and set of points. The rules vary widely on whether they can be cashed out, transferred, or with whom they can be redeemed against. Bonus point awards often take 6-8 weeks to post to your account after meeting the minimum spending, so if you are pressed for time, you may not be able to capitalize on those sweet bonuses. The moral of the story is, have a clear goal on what you want points for.

Who Should Absolutely NOT Churn

If you have ever carried a credit card balance, if you have ever been late on a payment, if your credit score is below 720, if you have ever had a library fine for returning a book late, credit card churning is NOT for you. You need to be meticulous!

Getting Our Toes Wet

We have plans to travel to Costa Rica later this year, so our goal is to reduce the cost of that trip with credit card churning.

This morning after doing plenty of research, I applied and was approved for the Capital One Venture card. I chose this card for several clear reasons.

The Venture card was one of the only cards that let you apply points retroactively (within 90 days) against transactions in your statement history. This is very important due to the timing of the trip we plan to take. If you add up the 3 months of spending to reach the min spend, and then an additional 2 months to have the bonus points post, you are already at five months from now to when you have points that you can use. Assuming that you book your airfare at the recommended 6 weeks pre-travel, you are looking at almost 7 months lead time from applying to a card to when your trip is going to be.

Another reason to go with Venture is the flexibility of using points. Any transaction that posts as travel can be redeemed against. You are not locked into a particular airline or hotel chain.

The minimum spend was within our capabilities. There are some fantastic business card sign up bonuses out there and some bigger personal bonuses, but they all have higher min spends. As a frugal family, we just don’t spend that much to meet those higher limits.

The 2x miles for every dollar spent means that the actual cash value will be ($3000 min spend * 2) + 40,000 bonus = 46,000 points = $460 in travel reimbursement. If Shae also signs up for a card that will be $920 of ‘free’ travel.

I applied online and was approved right away. Satisfyingly, my free account with Credit Karma sent me an email almost instantaneously informing me about the hard inquiry.

As expected, my credit score took a hit.

Keeping calendar reminders and detailed records is a must.

I will have to do a follow up post when/if we succeed in our first credit card churn. I am a bit concerned about meeting the min spend on two cards, but if we do some of the home improvement projects we have been considering, it shouldn’t be a problem.

Leave a comment if you have churned before or if you have a question about churning.