Whittling Down Our Paychecks to Save on Taxes

Tis the season to file tax returns for 2016. This is the first year we paid someone else to do it.

Taxes are the largest financial burden that you will shoulder throughout your life, even more so than buying a house or car. You get the same amount of government services as your neighbor does regardless of who pays more, so I am in the firm mindset of paying as little as legally possible.

My tax idol is the Root Of Good blogger. He had a great write up a couple of years ago about paying $150 of income tax on a $150,000 income. I’ve linked to it before, but here it is again because it is a must read for anyone looking to downsize their tax burden.

2016 was the first year that we were able to ‘max out’ all of our tax sheltered retirement accounts. I ran the numbers and thanks to that saver mindset we managed to avoid an enormous tax bill.

So how exactly did we do it?

Let’s run through the approximate numbers.

Our combined gross income from day jobs was about $133,000. Shae contributed the employee maximum ($18,000) to her 401k plan. I also contributed the maximum to my employee 401k plan. As an added perk to being self employed, I also get to put on the hat of the employer and contributed another $8,000 to my 401k plan.

Our combined gross income from day jobs was about $133,000. Shae contributed the employee maximum ($18,000) to her 401k plan. I also contributed the maximum to my employee 401k plan. As an added perk to being self employed, I also get to put on the hat of the employer and contributed another $8,000 to my 401k plan.

Shae has good benefits, and one of those is a flexible spending account for dependent care. She was able to tuck away $5,000 into that account tax free. Health and dental insurance also come out of the paycheck before taxes are applied, so that was another $3,100 and $350 respectively.

With all of those pre-tax deductions in place, our taxable salaries shrunk down to $80,550. From there, we have to start adding back some side income. We made $1600 of taxable interest by churning bank account bonuses. Our brokerage account kicked off $800 worth of dividends from VTSAX (Vanguard Total Stock Market Mutual Fund). $750 of those are qualified dividends and depending on your income level don’t get taxed. We also had rental income for the first time thanks to the addition of our first apartment building. We only owned it for 2.5 months in 2016, so it is just a glimpse. While on paper the $150 profit seems paltry, that comes after the magic of depreciation write offs. We were able to write off around $900 worth of depreciation for the building because in the eyes of the IRS, all buildings will be worth exactly $0 in 27.5 years. The secondary ‘hidden’ profit that has not been realized yet is the $400 of mortgage principal that was paid off in 2016.

Rounding out the additions and subtractions, we had $2300 in long term capital gains from selling off a chunk of our VTSAX investment to put a down payment on the apartment building. Like qualified dividends, if you can stay in the 15% tax bracket, you don’t have to pay taxes on LTCGs. We also fully funded each of our IRA accounts, so that is another $5500 x 2. Finally, I was able to deduct a portion of my self employment tax. It sounds like a sweet deal, but self employed people still get royally screwed in taxes. Normally you as the employee pay half of your Medicare and Social Security taxes and your employer pays the other half. Self employed folks get to wear both hats and foot both bills so this deduction is a little way to partially offset that.

In the end we finally get to the Adjusted Gross Income, AGI, of about $71,400.

From there, we get to deduct the Standard Deduction and 3 Personal Exemptions. With the addition of Frugal Girl in 2017 we should pay even less next year!

Taxable income comes in at $45,900 and the tax is about $5,600. We get one last hurrah before the cash register dings and that is in the form of a $1,000 child tax credit. Apparently the government wants us to have kids.

There you have it, $4,600 of income taxes on $133,000 gross income.

Now, the important question and why I bother getting onto this soapbox to ramble on about tax sheltering your hard earned money – How much would we have had to pay in taxes if we didn’t contribute to 401ks, IRAs, and Dependent Care accounts? Let’s run the numbers again with those key differences highlighted.

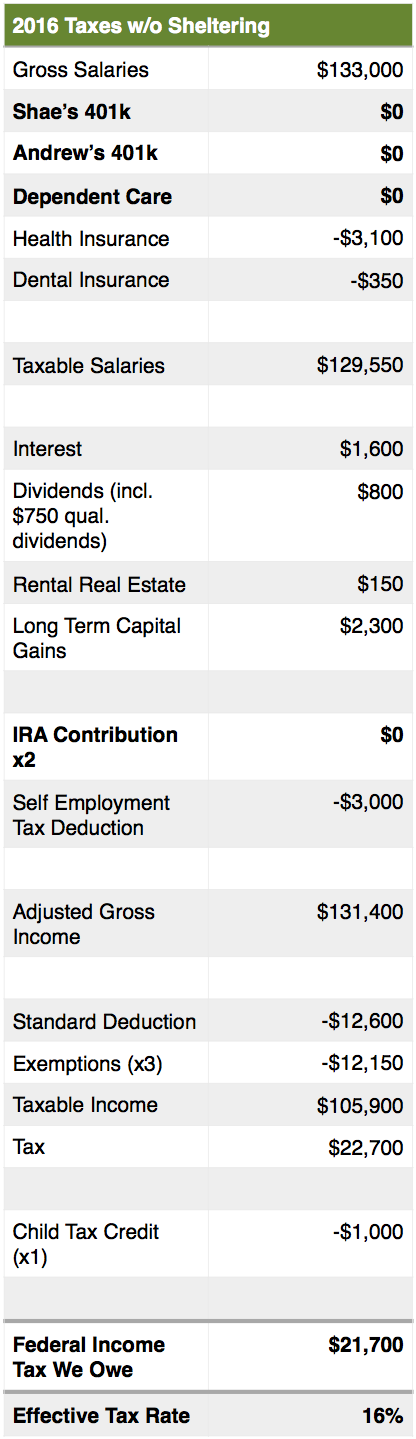

The gross salaries stay the same, but now the 401k’s and dependent care go unfunded. We really enjoy that big fat paycheck, but it isn’t as rosy as it may seem. The tax man cometh.

The gross salaries stay the same, but now the 401k’s and dependent care go unfunded. We really enjoy that big fat paycheck, but it isn’t as rosy as it may seem. The tax man cometh.

In the hypothetical, we also ignore setting up and contributing to IRAs. Our adjusted gross income has ballooned from $71,400 to $131,400. This is bad. We just moved from the nirvana 15% tax bracket where Uncle Sam is willing to give us a break to the 25% bracket where we need to ‘pay our share’. Suddenly qualified dividends and long term capital gains are now taxable. Working down the numbers we eventually come to the conclusion that the unsheltered strategy leaves us with a tax bill of $21,700. By using tax advantaged accounts, we saved $17,100 in federal income taxes. The effective tax rate jumps from 3.5% to 16%. OUCH!

It is practically a “max out one 401k and get one free” kind of deal. BOGOs on retirement plans. I’ll take 7 please!

Even with our usage of tax sheltered accounts we still paid boatloads in Social Security and Medicare taxes. At least with those you’ll likely see anywhere from 60-80% of it returned to you unless you die early. I also like to pretend that those payments go directly to our parents. It makes it a little easier to stomach when you think it is going to someone you know.

It took us years of concentrated effort to get to the point of maxing out retirement accounts, so don’t get discouraged if it seems a long way off or impossible. Even contributing an extra 1 or 2% of your paycheck is a big help and often times the easiest way to ramp up is to tuck away any bonus or promotion money.

Anyway, I just wanted to show a real life example of the power of putting away money into tax advantaged retirement accounts. We made a lot of mistakes on our way here and there is still a lot for us to learn. I hope it is useful for someone and if you have any tax tips that I should have mentioned please leave a comment!