Merry belated Christmas. We had an enjoyable time getting away from work for an extended weekend. Driving home we passed through several rain fronts, saw one 18 wheeler tipped over into the ditch from high winds, and witnessed many flooded areas. This morning a layer of freezing rain had coated all of the trees and the extra weight had caused many limbs to break off.

Shae noticed some water seeping into the basement, but nothing to be concerned about. The much more alarming discovery was when I went into the attic to check mouse traps. On my way down I noticed two very wet patches of floor where there shouldn’t be water.

On closer examination it appeared that water was coming into the house along the chimney and wicking down along the nearest rafter. I checked the bedroom below and sure enough there was some water discoloration on the ceiling. 🙁

Our roof was just put on two years ago, so I gave the roofer a call. He said that he would come around to look at it when the weather cleared up and it was safe to walk on the roof. He didn’t get any arguments from me, there is no way I would ask someone to walk around a steep icy roof.

There was still a slow persistent drip that needed to be dealt with to prevent any additional water damage. I can’t fix it from the outside, so the best I can do is divert that water to where I want it to go. In this case, a bucket. The best way I know how to do that is to create a wick. I nailed a rag into the rafter to interrupt the flow of water.

The water now flows down the rag and drips into the bucket. Voila, one MacGyver band aid.

and not a creature was stirring, not even a mouse because I just bought eight more mouse traps. If you recall, we have a bit of a mouse problem in our house as they have set up shop in the drop ceiling above our bed. Ewwww. Anyway, while I was at the store I perused their selection of 50% off Christmas decorations. This year our various strands of decorative lights had all given up the ghost and I am way to frugal to pay retail. At 50% off though I caved and bought a few strands of Christmas lights to do some last minute decorating. I figure in two days everything will be at 75% off so that would be the ideal time to stock up for next year.

Today, with Shae’s help I also finished making our homemade ravioli that we are giving away to friends and neighbors.

So far we have made a basic spinach & ricotta, butternut squash & gorgonzola, butternut squash & goat cheese cranberry, and our final most refined one was sweet potato & gorgonzola ravioli. We experimented with different dough recipes, rest times, rolling thickness, and cut out diameters before finding what we considered to be a tasty ravioli. I’ve made over 250 ravioli and at 2 minutes a piece it has definitely been a gift from the heart. Next year it may be back to easy and quick sugar cookie cutouts. Now that’s a sentence I’d never thought I would hear!

Here is one last frugal tip before I sign off and enjoy our traditional Christmas duck. If you are driving, make sure that your car tires are fully inflated. Under inflated tires reduces gas mileage and prematurely wears the tire. I checked all four tires on our car and found that they all needed some topping off.

Merry Christmas to all and to all a good night (except for those damn mice).

I read an interesting blog post about a month ago that talked about the effect of early retirement on social security. The writer concluded that retiring early on a high income was essentially the same as working longer at a lower income. In essence, the total amount of income is more important than time in the system.

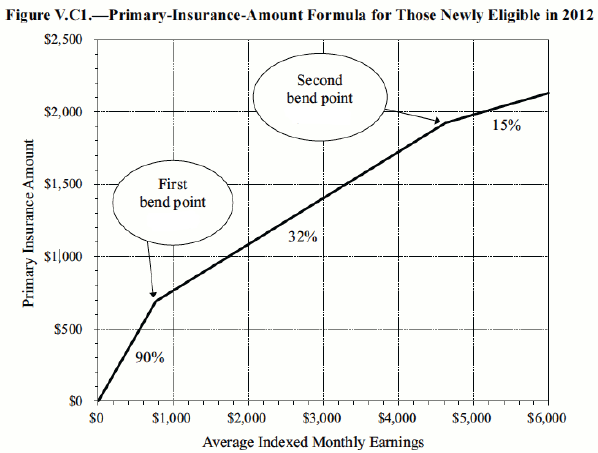

The reasoning behind this is how social security payments are calculated. The SSA, Social Security Administration, uses a formula to calculate ones benefit. That formula works off the PIA or primary insurance amount. The PIA formula uses a sliding scale and the average indexed monthly earnings (AIME).

Confused? Good. Then we were in the same boat the first time I read through this as well.

An example and charts will help explain the whole mess.

AIME

For starters we have the AIME, average indexed monthly earnings. Simply put, this number is how much you have earned in a 35 year period divided by 420 (35 years * 12 months). If you made a million dollars ($1,000,000) over the course of 35 years your AIME would be $2381 (they get rounded to the nearest whole dollar).

If you work more than 35 years, the lowest working year incomes are tossed out. If you work less than 35 years (early retirement) then the empty years are filled with zeros and that drags your AIME down.

Finally, in order to qualify for SS, you have to earn 40 work credits. You can earn up to 4 credits per year. To simplify, you have to earn money for at least 10 years to qualify for your own SS benefits (non-spousal).

You can look up your current work credits and earnings income on ssa.gov.

Now that we have an idea of what AIME is and what your AIME number could be, let’s see how the PIA formula plays out.

PIA

PIA works on a sliding scale. The first $856 of your AIME pays out at 90%. The amount of AIME between $856 and $5157 pays out at 32%. Anything above $5157 is paid out at a measly 15%. Graphically, it would look something like this:

Let’s consider two hypothetical men Mr. Management and Mr. Pleb. Management has done quite well for himself and his AIME is $6000 ($2.5 million earned over 35 years). Pleb has an AIME of $3000, half that of his middle management boss.

Using the PIA formula we can figure out the social security benefit for each man.

Mr. Management would get:

($856 * 0.9) = $770. This is before the first bend point

Plus

($4301 * 0.32) = $1373. This is between the two bend points

Plus

($843 * 0.15) = $126. This is after the final bend point

His total benefit would be $770 + $1373 + $126 = $2269/mo

You can see how the sliding scale makes the first $850 yield so much more than the last $840 dollars (770 vs 126). Social Security was designed to be a progressive system and is inverse of our progressive income tax system (the rich pay more and get less).

How about Mr. Pleb?

($856 * 0.9) + ($2144 * 0.32) = $1456/mo.

Mr Pleb made half as much as his boss, but will get more than half in social security.

How is this Useful?

Now that we know how the system works, we can game the system. It should be obvious that reaching the first bend point is critical to maximizing ones benefit. It should also be apparent that exceeding the second bend point is rather pointless in terms of benefit returns.

To fill up the first bend point, you’ll need to earn $359,520 over the course of 35 years (~$10k/year). It doesn’t matter if you earn 10k a year for 35 years or 360k in one year and nothing in other 34 years. Your SS benefit will be the same.

Social Security lacks returns once you cross over $2,165,940 of earned income (~$62k/year).

To game the system, try to earn as closely to 2.1 million as possible. Once you’ve made that, you can stop asking yourself if working longer is worth it for a bigger SS check. If you don’t make it to that amount, don’t sweat it. The really important bucket to fill is that first 90% payout.

With the end of the year in sight, it is time to do our annual tax forecast. Shae and I like to gather up our numbers and estimate how much of a tax liability we will have in April. Now is a good time to do it because there is still time to make adjustments to IRA contributions and 4Q estimated payments (due in January) for my business.

A really simple tool to use is Intuit’s TaxCaster. Intuit is the company that makes TurboTax and Mint.com. After putting in our numbers, it looks like we’ll end up overpaying if we stay the course.

Our total tax bill will be about the same as 2014 even though we made more money in 2015. We were able to squirrel away more income into tax deferred accounts such as 401ks and IRAs this year. Self employment tax continues to be a major bane as there are no loop holes to get out of it. Ugh!

For 2016 our goal is to drastically reduce our tax liability by fully funding our retirement accounts. This year we finished paying off our house so we shouldn’t need as much cash flow in the coming year. If you want to read a truly inspirational account of one couple paying a meager $150 in income taxes on $150,000 income go read this blog post here. Spoiler alert, the answer is to shove as much money into tax sheltered accounts as possible and have lots of kids (ok, just 3).

Yesterday was a rainy day, so a trip to the Children’s Museum was in order. Frugal Boy is old enough now that he would actually enjoy it and not put every single toy in his mouth. Our museum offers memberships for $95 that give unlimited visits for the entire family for 1 year. That isn’t a bad price considering a daily ticket is $7 per person two and older. We splurged and got the membership plus level for $130. The extra cost includes one free guest pass for each visit and access to the ACM reciprocal network.

Now we have 12 months to get another $109 worth of value out of our memberships. It should be good motivation to get out of the house and go places.