It has been a little under 2 months from our first churning credit card application (read more about that here). In case you have no idea what I am talking about, credit card churning is the process of signing up for credit cards with the sole goal of collecting hefty signup bonuses from the bank. We have a trip planned for Costa Rica this summer and we wanted to see just how much money we could knock off the total bill.

The first credit card that I targeted was the Capital One Venture card. I just completed the requirements to get the bonus for that card and the 40,000 bonus points posted soon after.

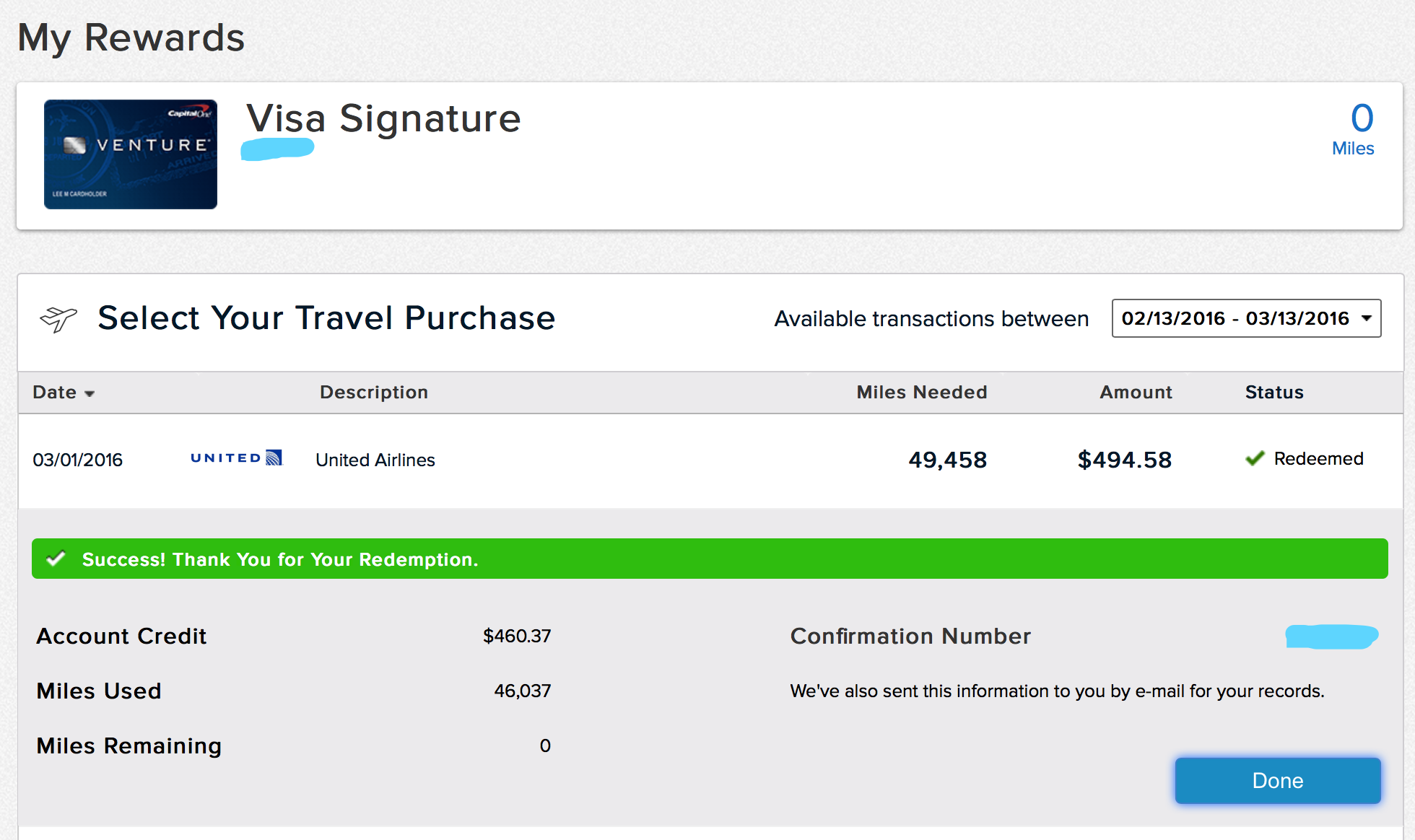

I was able to redeem the full point total against a plane ticket to Costa Rica to knock $460.37 off a $494.58 ticket. 93% off airfare isn’t too shabby!

Shae also got into the game and completed the requirements for the Barclaycard Arrival Plus. When we purchased airfare, we did it in two separate transactions so that we would be able to redeem multiple credit card bonuses against the cost.

Barclaycard Arrival + is a very similar setup to the Capital One Venture card. 40,000 bonus points are awarded for spending $3k in 3 months. One of the small differences between the two is that the BA+ card can only be redeemed in increments of 2500 points. Shae was able to get $450 applied towards a $494.58 airfare.

I am quite pleased that with two cards we were able to save $910.37 in travel expenses. That will go a long way to reducing the cost of our Costa Rica trip this summer.

But Wait, There’s More!

I’ll admit it. I got hooked. Credit card churning has been an enjoyable distraction for me. If you read the fine print, have clear goals, and a modicum of self discipline you can rack up quite a bit of ‘free’ money.

My spreadsheet has grown considerably from that initial blog post two months ago. Yes, it is color coded now according to the card issuer. Click on the image below to see a bigger more readable version.

In total we have applied for 8 cards.

Chase Freedom

- Annual Fee: $0

- Bonus: $150 + $50 for referer

- Min Spend: $500

- Min Spend Deadline: 3 months

I already have this card and it is one that I use on a monthly basis. Chase keeps sending me emails to pimp this card out to my friends and family. If someone signs up for the card through my referral link, I get $50. No, I won’t put the link on this blog.

Shae signed up through the link however so this card should net us an easy $200 and because it has no annual fee, she can hold onto it forever.

BankAmericard Travel Rewards

- Annual Fee: $0

- Bonus: $200 statement credit

- Min Spend: $1000

- Min Spend Deadline: 3 months

Both Shae and I applied for this card. Shae was approved and I was denied. Ironically, because I didn’t have enough credit card accounts. Hehehe. The plan is to use the card and bonus for Costa Rica lodging.

Chase Sapphire Preferred

- Annual Fee: $89, waived first year

- Bonus: 55000 Ultimate Reward Points (between $550 and $687)

- Min Spend: $4000

- Min Spend Deadline: 3 months

I got this card for future travel. We plan to meet the min spend by paying our property taxes with it. Yes, our property taxes are almost $4000/year. We might as well get a bonus while we rip off the tape.

IHG Rewards Club

- Annual Fee: $49, waived first year

- Bonus: 60,000 points + $50 statement credit OR 80,000 points

- Min Spend: $1000

- Min Spend Deadline: 3 months

I got this hotel credit card because it is a surprisingly good value. In addition to the one time bonus, you also get a free night every year starting on your second year of membership. Essentially, you get a $49 night at any IHG hotel. The lower tier hotels start free nights at 5-10k points. 80k reward points would be enough for around 8 free nights. If you figure those are $80 nights normally, then the bonus is worth around $640.

Chase Total Checking

- Monthly Fee: $12 unless criteria are met

- Bonus: $300

- Bonus Requirement: Make a direct deposit of at least $500.

- Bonus Req Deadline: 2 months

This one isn’t a credit card! It is a checking account. The $300 bonus was a targeted offer that Chase sent me. They really want me to be a customer, so they offered a big bonus to lure me in. The requirements are pretty easy to meet. Open it up in branch with the targeted coupon code, dump $1500 in to satisfy the monthly fee requirements, and then make a direct deposit of $500. Wait 6 months to satisfy the fine print and then close the account. Abbra Cadabra, $300 for about 3 hours of work.

Wrapping Up

All told we are looking at about $3200 in bonus churning provided that we meet the various requirements and are able to optimize the bonus redemptions. I like that I can do most of this from my computer and it doesn’t hurt that we can stick it to big companies in the process.

Speaking of Which

Did you see the credit limits that we were approved for?! Holy crap. No wonder why Americans are in debt up to their eyeballs. It is so easy to get ridiculously high credit lines. Why in the world do credit card companies think that handing out $127,900 of available credit to a couple of twenty year olds is a good idea. The morbid reason is simple, the companies are hoping we self destruct and spend more than we can pay off. If we fell into that trap, then the companies make money in insanely high APRs ranging from 14% all the way up to 22%. These companies want people to pay the minimum. So sure, give Andrew a credit limit of $25,000 and hope he screws up and becomes a wage slave. That is why I have zero empathy and zero remorse from milking these card issuers for big bonuses. I’ll play the game, but I’ll play it on my terms.

Whittling Down Our Paychecks to Save on Taxes – Frugal Living

[…] From there, we have to start adding back some side income. We made $1600 of taxable interest by churning bank account bonuses. Our brokerage account kicked off $800 worth of dividends from VTSAX (Vanguard Total Stock Market […]